(Donald Trump with Elon Musk, Tulsi Gabbard, RFK Jr, and Mike Johnson Credit photo: from Office of Speaker Mike Johnson – Public Domain )

President-elect Donald Trump declared that Canada should become the “51st state” of the United States of America. He also repeats quite often that the U.S. should “buy Greenland” (Alexandra Sharp, “The 51st Star on the U.S. flag?”, Foreign Policy, December 19, 2024 and Anthony Slodkowski and James Pomfret, “Trump Greenland bid stirs debate in China about what to do with Taiwan”, Reuters, 15 January, 2025).

Meanwhile, Elon Musk, the multibillionaire techno-industrialist and adviser of Donald Trump, had a rough polemic with Justin Trudeau, the resigning Prime minister of Canada, via Twitter/X. (Anushree Jonko, “Musk mocks Justin Trudeau over Canada-US merger idea, says, “Girl…””, NDTV, 8 January 2025.

Those statements took place during the presidential transition. The transition team is dominated by a network of high level personalities of the tech and AI sector. It is the case, for example, of David Sacks, massive investor in tech who is the “Crypto and AI Czar” of the transition team (“Who’s Who in Trump’s new Silicon Valley entourage ?“, BestofAI, via Financialpost.com, 19 December 2024).

One must also note that vice-president J. D. Vance has a history as a venture capitalist in the tech business world. Among others, he is close to Peter Thiel, one of the most powerful tech billionaires, founder of Palantir (Erin Mansfield, “Peter Thiel and JD Vance: How Paypal founder boosted VP’s candidate political career”, USA Today, 17 July 2024).

As we shall see, confronting these declarations and the interests of the AI community reveals some of the main drivers of the Trump presidency political guidelines.

Greenland and Canada are of crucial importance for the development of the national AI industry. Indeed, the extremely rapid development of this sector consumes growing energy and mineral resources.

So, identifying Canada as a strategic target of its foreign policy makes perfect sense from a strategic point of view (REE Mineralisation in Greenland, Eurare).

So, we hypothesize here that President Trump guidelines about Canada and Greenland are also those of the AI/ strategic resources definition of the U.S. national interest at the start of his presidency.

In this article, we shall look at the way the “Trump II” presidency’s interest for AI development roots itself in the power networks of the Silicon Valley as well as in the development dynamics of the AI sector. Then, we highlight that the declarations about Canada and Greenland reveal the rising interest of the AI sector for energy and mineral resources. Finally, we investigate what those evolutions mean in geopolitical and strategic terms for the American “AI power”.

Donald Trump II and AI

We are f.AI.mily

The second Donald’s Trump presidential campaign appears as having been strongly supported by part of the tech industry, including AI, and some of their main figures. Among them, Peter Thiel’s network seems to be quite prominent.

Marc Andreesssen is another major figure in the network. He is a major investor in tech and AI companies, for example AirBnB, FaceBook or Coinbase among others. Marc Andreessen seems to be an active recruiter for the Trump administration (Sarah Mac Bride, “Here is a list of tech leaders joining Trump’s new Silicon Valley entourage”, from Bloomberg, Business Standard, 20 December, 2024).

If Microsoft, Facebook and Amazon have not been vocal about Donald Trump during the major part of the presidential campaign, some movements seem important to note.

Now, some of the members of this tech network will be part of Trump’s government. For example, David Sacks, an ex-employee of Peter Thiel and Elon Musk at Paypal, is going to be the White House “AI and crypto Czar”. Trae Stephens, ex-general partner at “Founder’s fund”, an investment fund in technology, including AI, created par Peter Thiel, may become deputy secretary of Defense.

Then, there is the dense network of relationships between Peter Thiel venture fund, that, among other things, invest in Elon Musk societies, as the “new space” company Space X as well as the Starlink satellite constellations. The Founder’s Fund is also investing in Palantir and in Anduril, a society specializing in combat drones (Dom Lim, “The Silicon Valley Sci Fi Complex: How Tolkien, Iron Man and PayPal Founders are shaping the future of defense AI“, Medium, November 10, 2024).

Factually, these people and the personal, corporate, institutional, political and financial networks that link them are literally representing vast tracts of the U.S. tech as well as AI industry sector. It is also interesting to note that major companies as, among others, Palantir, Anduril, Starlink are drivers of the AI militarization (Roberto J. Gonzalez, War Virtually, the Quest to Automate Conflict, Militarize Data, and Predict the Future, Oakland, University of California Press, 2022).

One could say that the omnipresence of Elon Musk around Donald Trump personifies the interdependencies between the rising interests of AI industries and of the U.S. national interest. Indeed, Elon Musk is part of the multiple networks that link Silicon Valley tech billionaires, as well as their industries.

Those networks also link those very people and industries to the U.S. national security and defense community ( Jean-Michel Valantin, “AI at War (1) – Ukraine”, The Red Team Analysis Society, April 3, 2024). Knowing that the military branch is a core part of the state, the militarization of AI also appears as a major dynamic of its institutional integration (Ian Morris, War, what is it good for ? : Conflict and progress of civilization from primates to robots, Farrar, Strauss and Giroux, 2014).

So, from a network analysis perspective, those companies are literally nodes that connect the AI industry to the military sector. They are drivers of the industrial, strategic, and operational implementation of the US national interest.

National A.Interest

As explained by Helene Lavoix,“The American national interest” is simple. Basically, it is about protecting the security of the American people (ISSG). It is further broken down, as explained in the NDS 22 factsheet, into three vital U.S. national interests:

“The protection of the American people, The expansion of America’s prosperity, The realisation and defence of our democratic values.”

Nowadays, the first and second item of this list appear as closely linked to the development of the AI sector.

Growth

Indeed, according to Statista Market Forecast, the U.S. AI sector knows an explosive growth. Its total size was 25.65 billion USD in 2020. Then, it was 54.87 billion USD in 2021 and 34.67 bn USD in 2022, which was a year of adjustment. Then it reached 37.23 bn USD in 2023 and 50.17 in 2024. The growth of the U.S. AI sector could reach 66.21 bn USD in 2025. If the sector keeps growing at this rate, it could reach 223.61 bn USD in 2030 (“Artificial intelligence – United States”, Statista).

So, still according to Statista, this rate of growth corresponds to 1.22% of the U.S. GDP in 2022 to 1.51% in 2023 and 3.23% in 2024. It could reach 5.13% in 2025. At this rate, everything being equal, the U.S. AI sector could be the equivalent of 14.19% of the U.S. GDP in 2030.

This growth goes hand in hand with the rising number of U.S. users. They were 48.13 million in 2020, 59.72 in 2021, 75.07 in 2022, 92.78 in 2023, 112.60 in 2024. Hypothetically, the number of U.S. users of AI may reach 138 million in 2025. In 2030, it could be 241.50 million people, on a total population of 350 million people (Statista, ibid).

The mammoth of semiconductors

This explosive rate of growth fuels an intense demand for semiconductors. This demand drives the transformation of Nvidia. This company is the main U.S. producer of semiconductors and, in 2024 it became one of the two most valuable U.S. firms.

In other terms, the U.S. AI sector is becoming a powerful economic engine. Its rhythm of growth is driven by the very particularity of AI technologies. Indeed, those technologies integrate each and every sector, from agriculture and transport to robotics, management, security, international influence and war (Hélène Lavoix, “ Smart agriculture, International power and national interest”, The Red Team Analysis Society, April 11, 2019 and Hélène Lavoix, “Exploring cascading impacts with AI”, The Red Team Analysis Society, May 17, 2023 and “Portal to AI-Understanding AI and Foreseeing the AI powered world”, The Red Team Analysis Society) .

Thus, it appears that the involvement of the AI sector in favour of Donald Trump also represents its involvement in favour of the policy guidelines of his administration.

From Greenland and Canada to U.S. AI

In this context, the interest of President Trump in Canada and Greenland appears as closely linked to the needs of the U.S. AI industry in electricity generation and mineral resources.

Indeed, the rapid growth of AI uses and its scale induces a formidable pressure on the U.S. electricity generation capabilities.

The energy gap

According to Goldman Sachs, the data centres demand for power was stable. Worldwide, -those infrastructures were consuming between 1% and 2% of the overall power. However, this demand could grow 160% by 2030. This spike is intrinsically linked to AI development. Indeed, if a Google Search consumes O.3 watt per hour, a single Chat GPT request consumes 2.9 watt-hour of electricity (“GS Sustain: Generational Growth: AI, Data Centres and the Coming US Power Surge”, Goldman Sachs, April 29, 2024).

Still according to Goldman Sachs, data centres already consume 3% of the U.S. power production. However, this demand may grow to 8% by 2030. In order to answer this demand, the U.S. will have to produce 47 gigawatt of incremental power capacity. Hence, as Hélène Lavoix establishes, the project of a “US nuclear renaissance” (Hélène Lavoix, “Towards a U.S. Nuclear Renaissance?” The Red Team Analysis Society, 15 October 2024).

Those energy needs are compounded with those of the uses of AI. Their growth is destabilizing the U.S. electricity market, which contributes to the need for a “nuclear renaissance” (Lavoix, Ibid.). Thus, the theoretical interest for the U.S. to have a better access to Canadian uranium, oil, gas and hydroelectricity (Helene Lavoix, “Uranium for the U.S. Nuclear Renaissance (2): Towards a global geopolitical race”, The Red Team Analysis Society 18 January 2025).

In this context, the interest of President Trump for Canada appears rooted in the U.S. equation of AI growth/ power demand / power generation. Indeed, Canada is a major producer of energy, through hydroelectricity, the shale oil and gas production of Alberta, renewanle energies, and its uranium mines (Hélène Lavoix, “Uranium for US Nuclear Renaissance- 1 : Meeting Unprecedented Requirements”, The Red Team Analysis Society, 27 November, 2024, and Ian Riach, “AI data centres are hungry for power and Canada is answering the call”, Fiduciary Trust Canada, 18 November, 2024).

The translation of the emerging energy needs of the AI industry into political discourse takes many forms. For example, it is worth quoting Eric Schmidt, co-founder of Google. During a conference at Stanford university, he declared that:

“ I went to the White House, and told them that we had to become Canada’s best friends,…. Because they have… LOTS of hydropower and we (the US) do not have enough power… So, the alternative is the Arabs… but they’re not going to adhere to our national security rules… whereas US and Canada are part of a giant continent…”.

Eric Schmidt, “Not deleted one second – Ex Google CEO Schmidt was invited to give a speech (confidential meeting).

As it happens, accessing the White House is possible for Eric Schmidt because from 2018, (during the first Trump presidency), to 2021, (during the Joe Biden Presidency), he was chair of the National Security Commission on AI. In this capacity, he is a prominent voice in the field of co-integration of the AI sector and of the Federal State, the national security community and of the American civil society. One must note that one of the main recommendations of the commission is that the “US Government must embrace the AI competition and organize to win it”.

So, it appears possible to interpret the declarations of President Trump about Canada becoming the “51st state” of the U.S. federation as an “official translation” of the strategic importance of Canada for the development of the U.S. AI industry and power. It also translates the growing concern of the AI sector about accessing enough energy to support its growth.

A (very) material AI world

The material needs of the U.S. AI sector do not stop at energy. This industrial sector needs massive amounts of rare earths minerals. Those elements are essential in order to produce the very semiconductors needed for AI computers. However, the main mines and refining capabilities of these minerals have been developed in China. This situation has created a de facto dependency between countries and companies needing rare earth elements and their refining and China (Inkster, ibid).

Those minerals are a basic need for semiconductors production. Thus, for example, they are of vital importance for Nvidia. As it happens, Beijing is now imposing a ban on rare earth elements exports as well as on rare earth processing technologies to the US.

In this context, when president-elect Trump expresses an interest in “buying Greenland”, it is worth noting that there are important deposits of different rare earth elements in Greenland “Why the world is turning to Greenland rare earth metals?”, Innovation News Network, Innovation News Network, 03 August, 2023).

As it happens, Greenland is in the European-Danish legal sphere. However, the country is part of the U.S. defense sphere since 1941. Indeed, Greenland hosts the Air Force / Space force Pittuflik base, also known as the “Thule base”.

So, in the AI age, the rare earth elements deposits are strongly increasing the strategic value of Greenland for the US. His declarations are the way President Trump translates this dynamic into a political guideline.

The President of U.S. AI power

In other terms, there is a very strong possibility that the second mandate of President Donald Trump will see the strategic integration of the AI sector to the status of the U.S. as a 21 century Great power.

Towards the AI State

This dynamic is already expressing itself in an institutional way, with the creation of the Department of Government Efficiency (DOGE). With Elon Musk as chair and Vivek Ramaswamy as co-chair, this presidential advisory commission will promote technology as a way to reduce the number of federal agencies as well as of employees.

The main mission of the commission is to lead “three major kinds of reforms: regulatory rescissions, administrative reductions and cost savings”. Some of the goal of the commission are to redefine government efficiency in a rapidly changing digital and technological context (Ross Gianfortune, “Proposed DOGE reforms target technology, efficiency”, GOVCIO Media Research, 01/06/2025).

In other terms, the DOGE will (try to) lead both the integration of current tech, i.e artificial intelligence, to the Federal State, while reducing regulation in the technological sector (Ross Gianfortune, ibid) . As it happens, these goals appear quite clearly aligned on the recommendations developed by the National Security Commission on AI, chaired by Eric Schmidt (Schmidt, ibid, see above).

This strongly suggests that there are continuities between the works of the commission that published its results in 2021 and the program of the DOGE in 2024-2025. This continuity appears especially In the sharing of the 2021 goals of the Commission that state the needs of the projection of the AI sector in the governmental institutions as well as in the fabric of the US society and the announced mission of the DOGE, that appear as an operational translation of these goals.

Towards AI geopolitical escalation ?

One must remember that these goals take place in the context of the rapid militarization and weaponization of AI. One driver of this dynamic is the US military demand for technology. Another is the competition with China, the other Great power. And China is also leading a rapid “intelligentization” of its military forces (Jean-Michel Valantin, “AI at War (2) – Preparing for the U.S China War ?”, The Red Team Analysis Society, September 17, 2024).

So, the second Trump presidency might very well be seen as the political structure that is going to produce the U.S. form of AI political power and governance. This may happen by channelling the AI revolution into the very workings of the Federal government

This AI channelling is already imprinting the process of definition of the US as a Great power geopolitical guidelines. Thus, this dynamic could become the U.S. political version of what Helene Lavoix defines as AI Power in an AI World ((“When Artificial Intelligence will Power Geopolitics – Presenting AI”, The Red Team Analysis Society, November 27, 2017).

Now, it must be seen how the U.S. AI power is going to interact with its allies as well as its enemies.

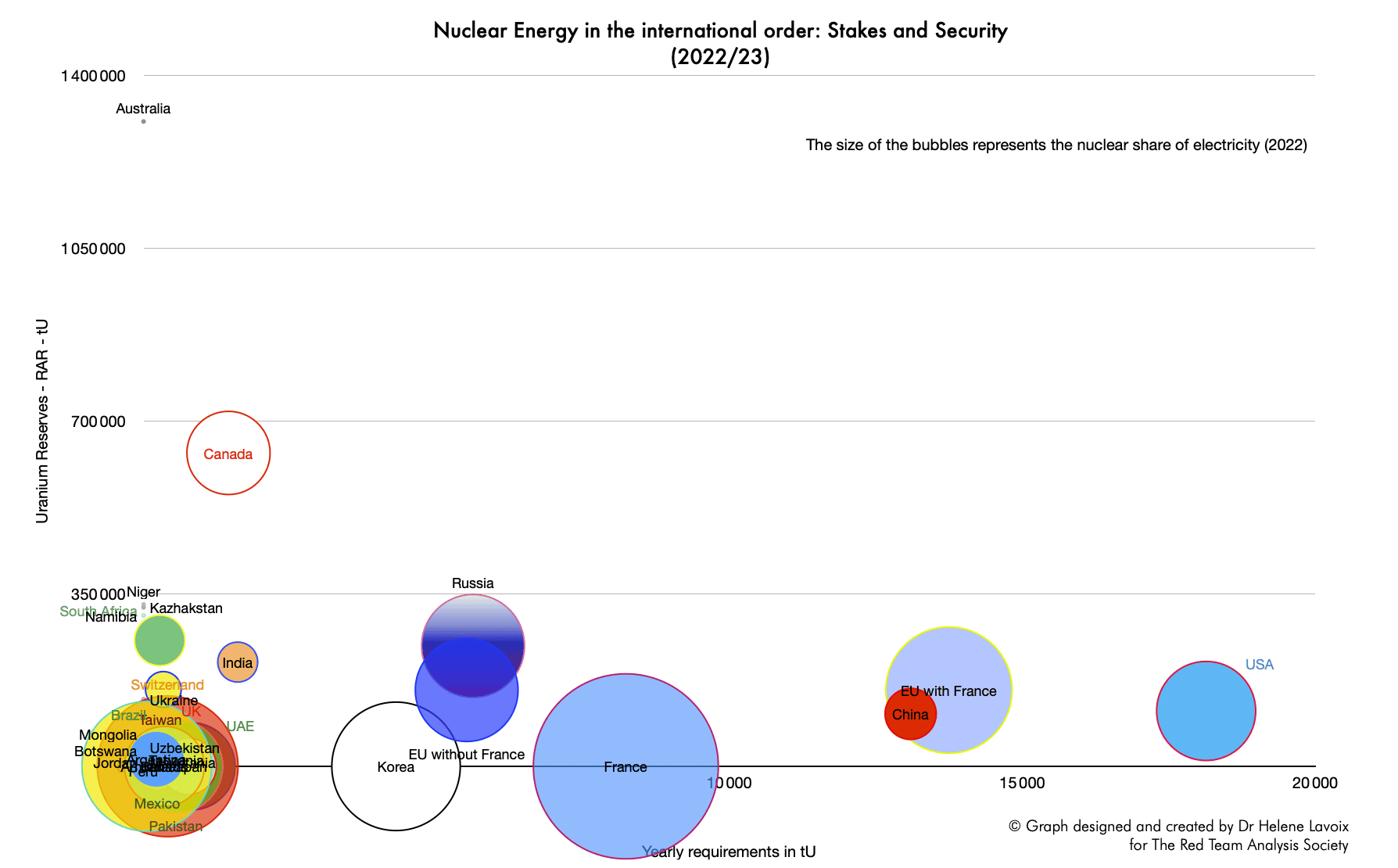

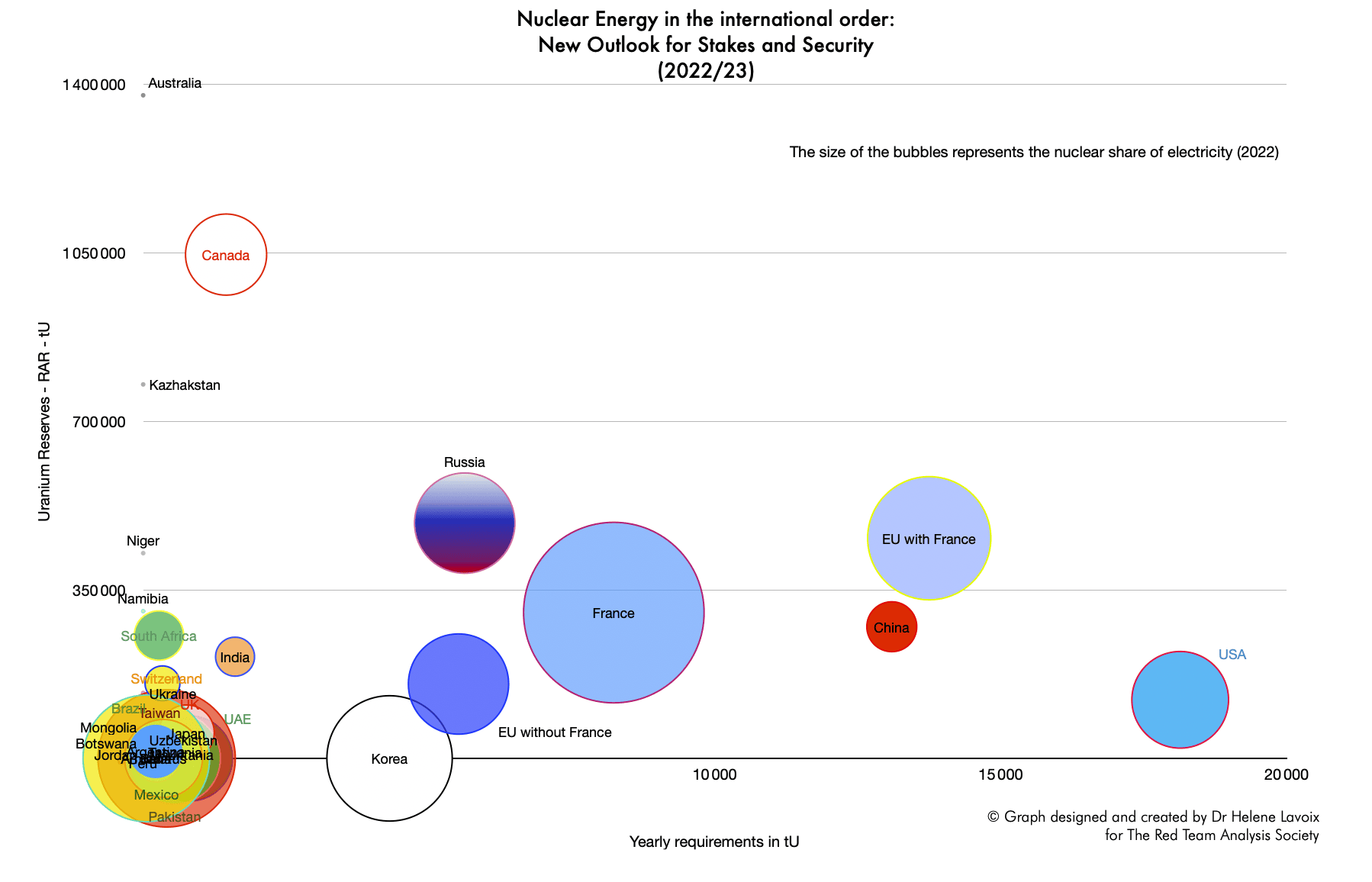

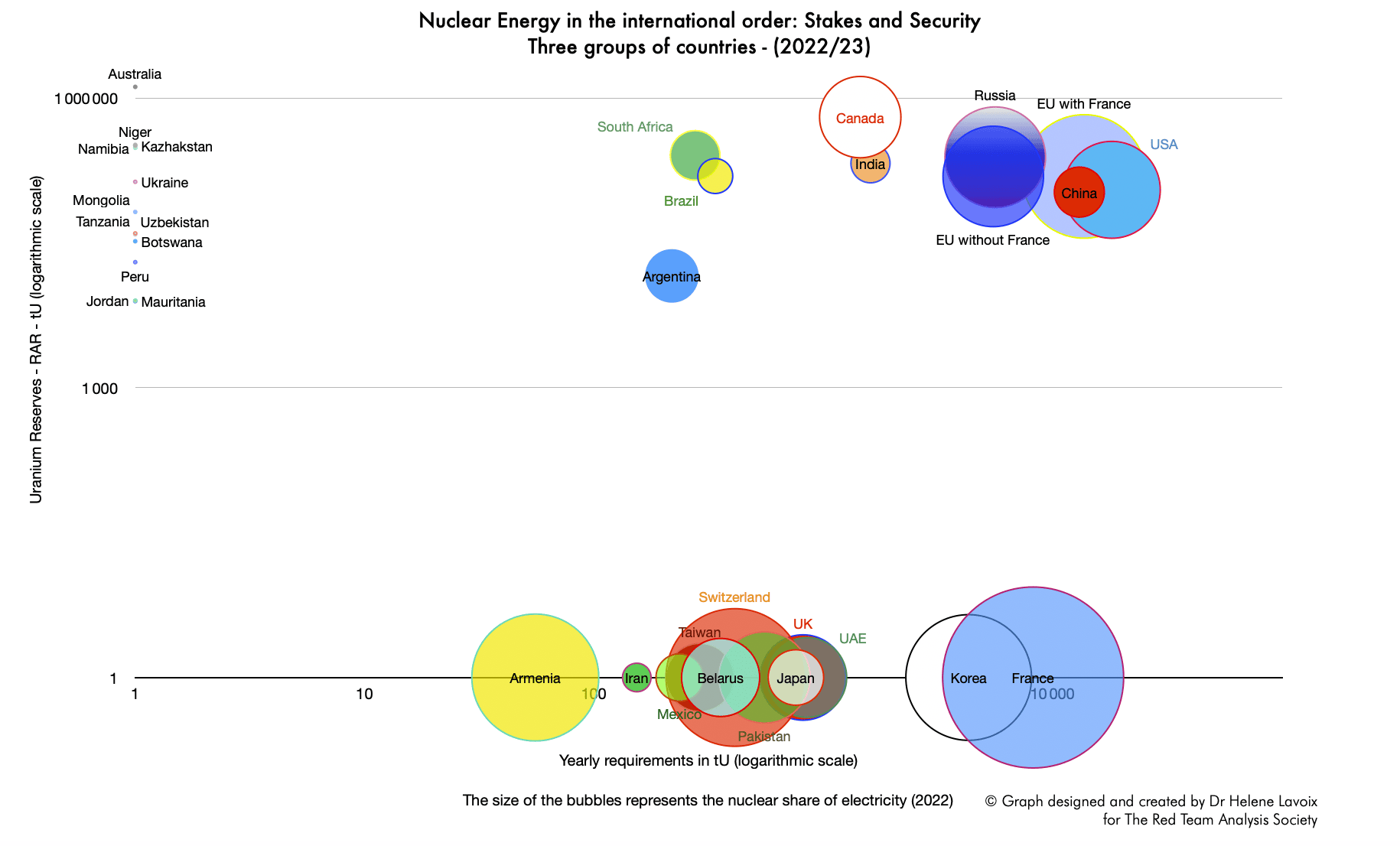

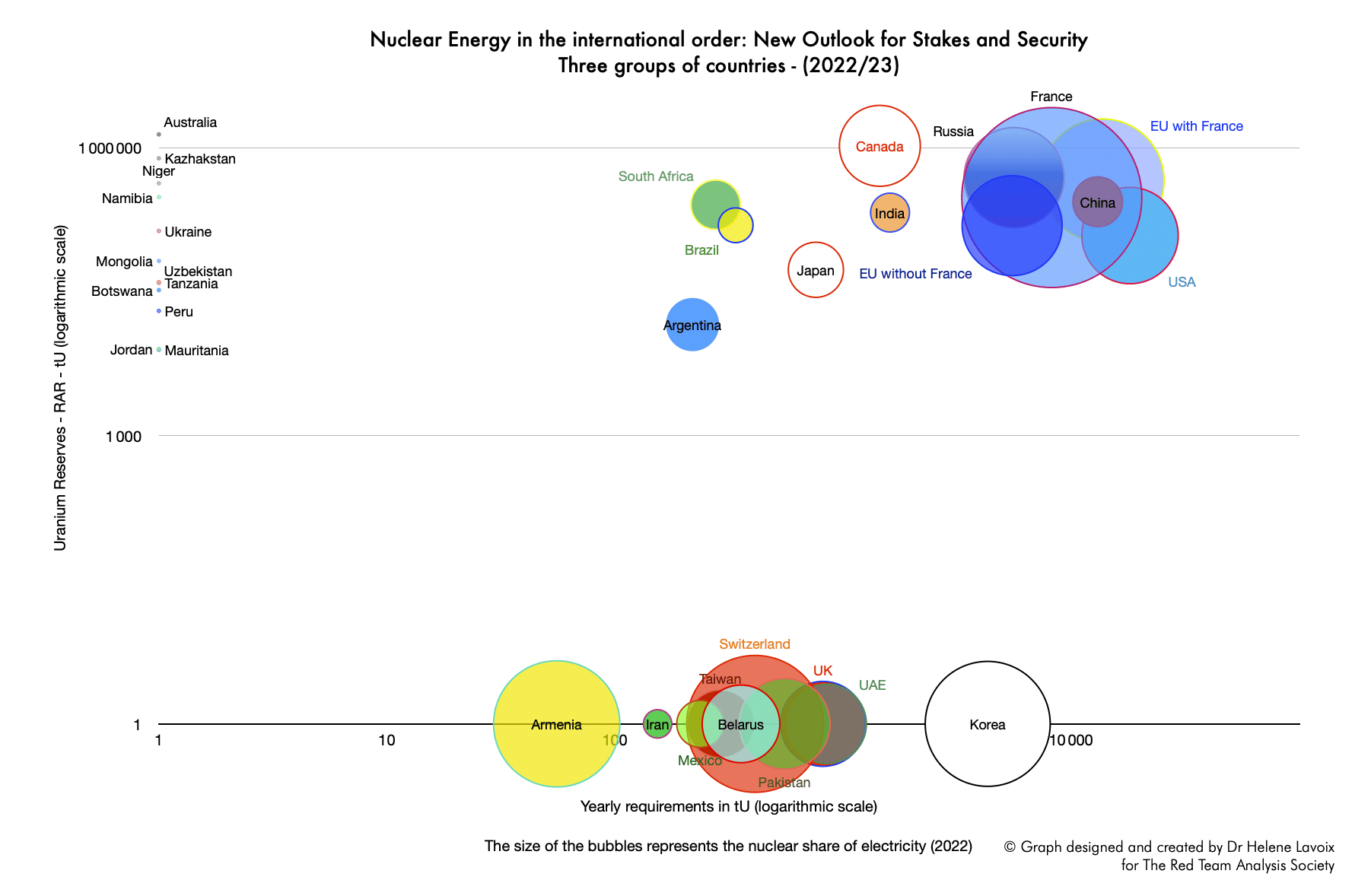

The uranium requirements created by the planned American nuclear renaissance are immense and unprecedented (see Helene Lavoix, “Uranium for the U.S. Nuclear Renaissance: Meeting Unprecedented Requirements (1)“, The Red Team Analysis Society, 27 November 2024). Yet, the production of uranium in the U.S., the American reserves and resources of uranium, as well as the involvement of American companies in uranium mining are all insufficient to allow the U.S. to meet its future needs in uranium (Ibid.).

The U.S. will thus need to increase its uranium supply overseas, probably through foreign companies. Hence, we need to look at the global uranium supply and demand situation. We need to do so while also accounting for the impact on global uranium supply of the potential new American uranium requirements.

Thus, first, we focus on the making of a global gap between supply and demand, stemming, notably, not only from U.S. uranium requirements but also from Chinese ones. Then, we highlight the major consequences of the global uranium supply demand gap, namely rising uranium prices, the necessity to bring about new mines and mills and a tough geopolitical competition for uranium. From there, finally, we identify future possible ways for the U.S. to meet its uranium requirements. We notably envision some changes of the norms of the international order, as already stressed by U.S. President Trump.

Nota: In this article, by resources [in uranium] we mean measured and indicated resources, i.e. those best assessed with the highest degree of “geological confidence” (see glossary).

The U.S. and China: The making of a global gap between supply and demand

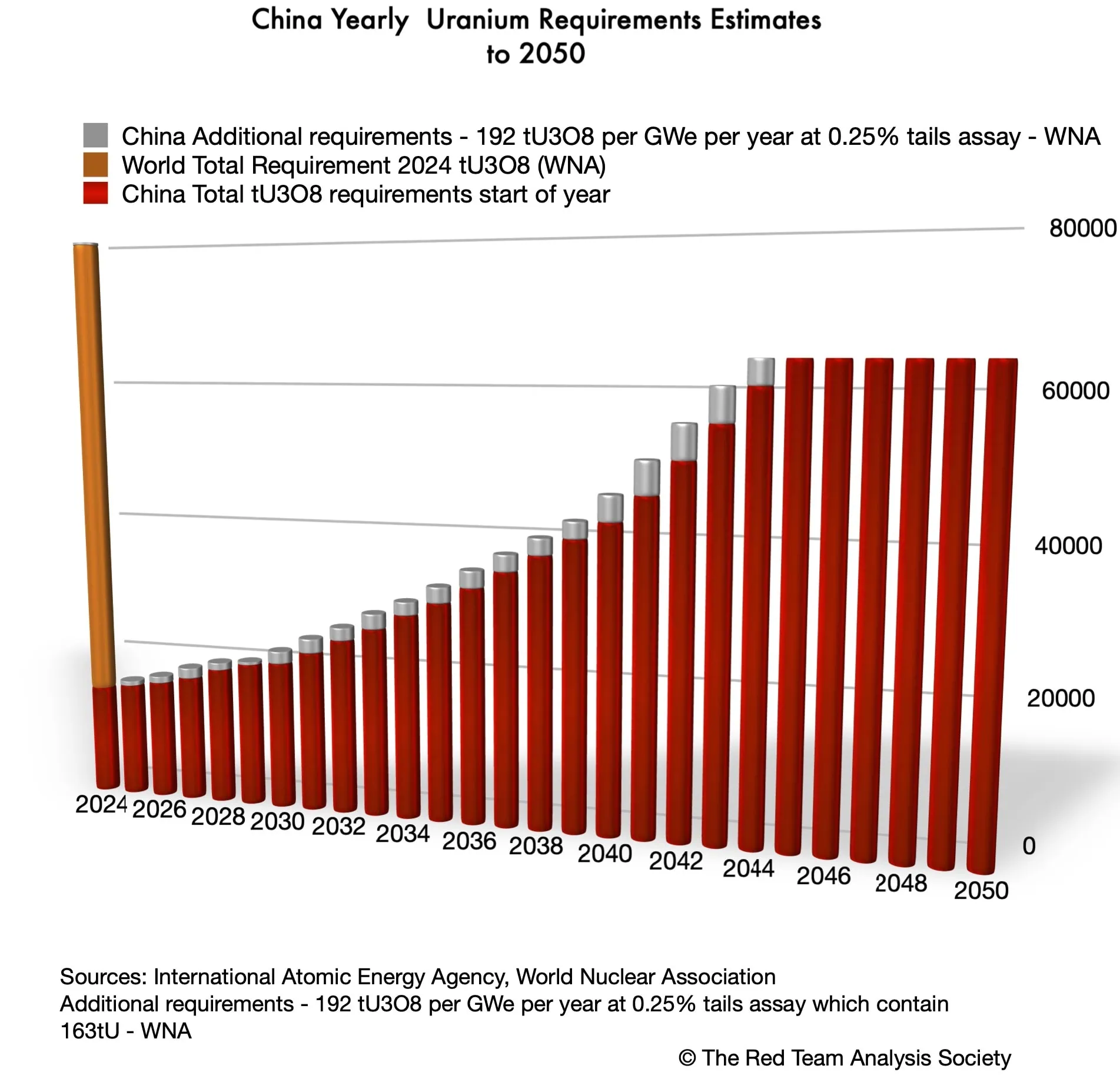

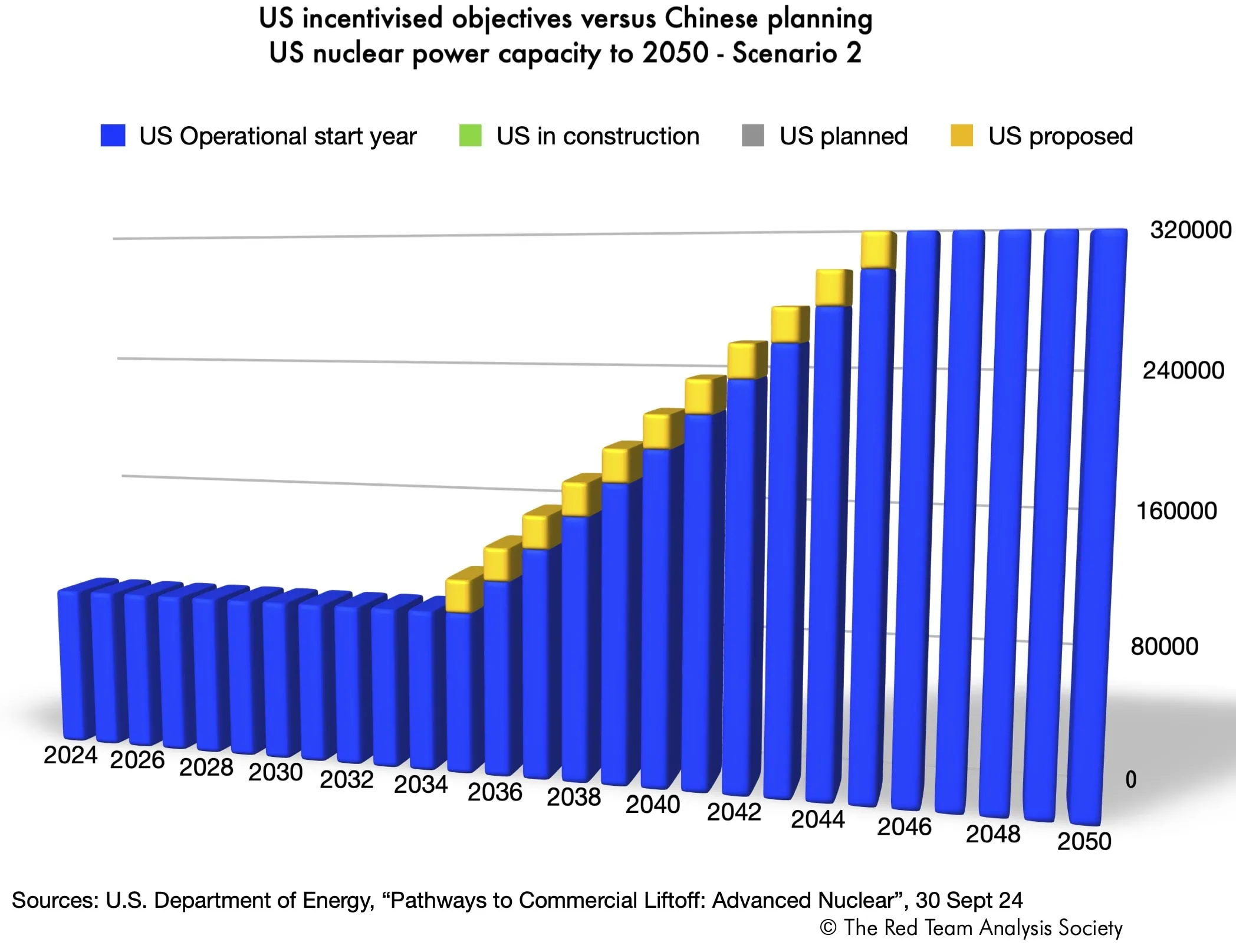

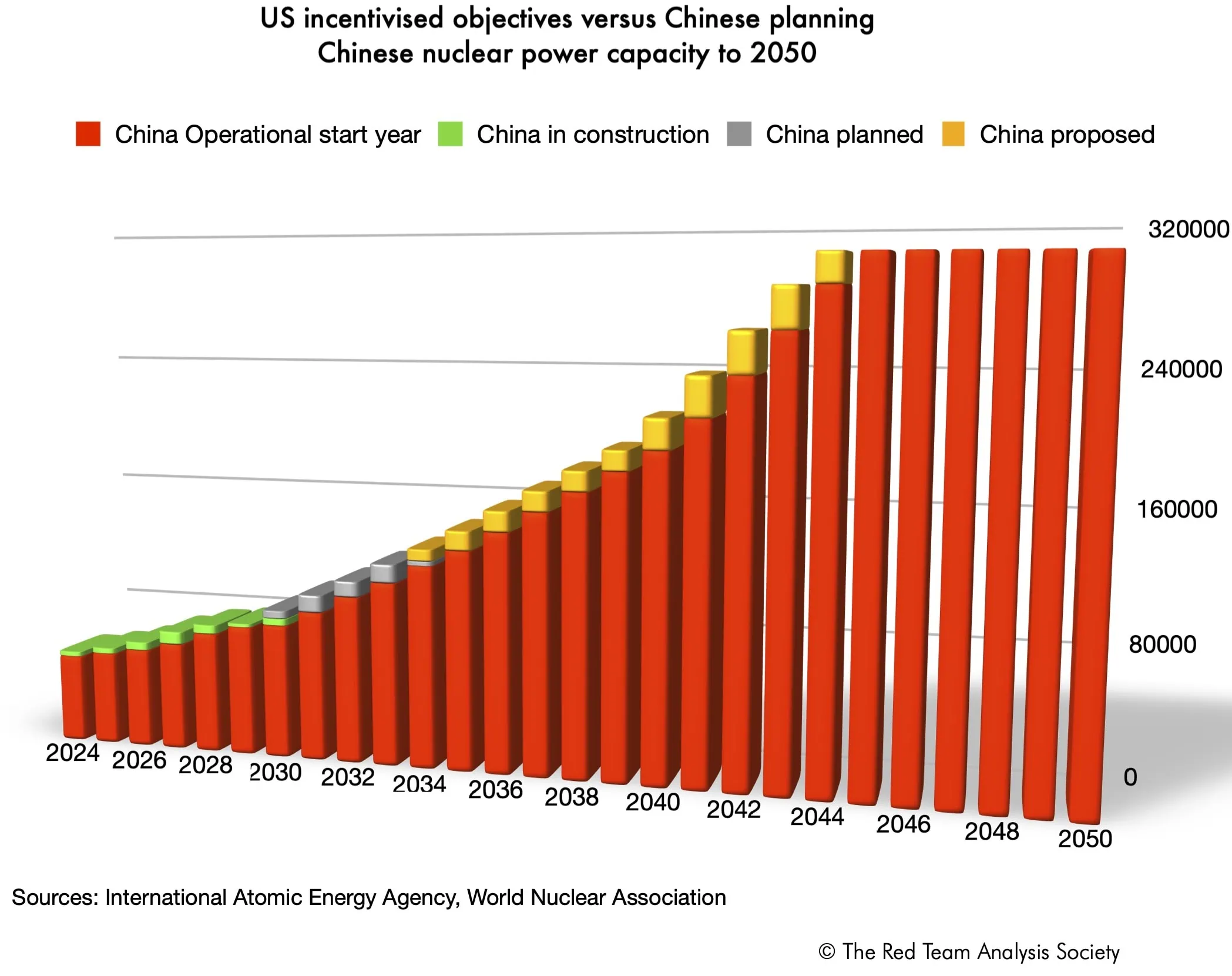

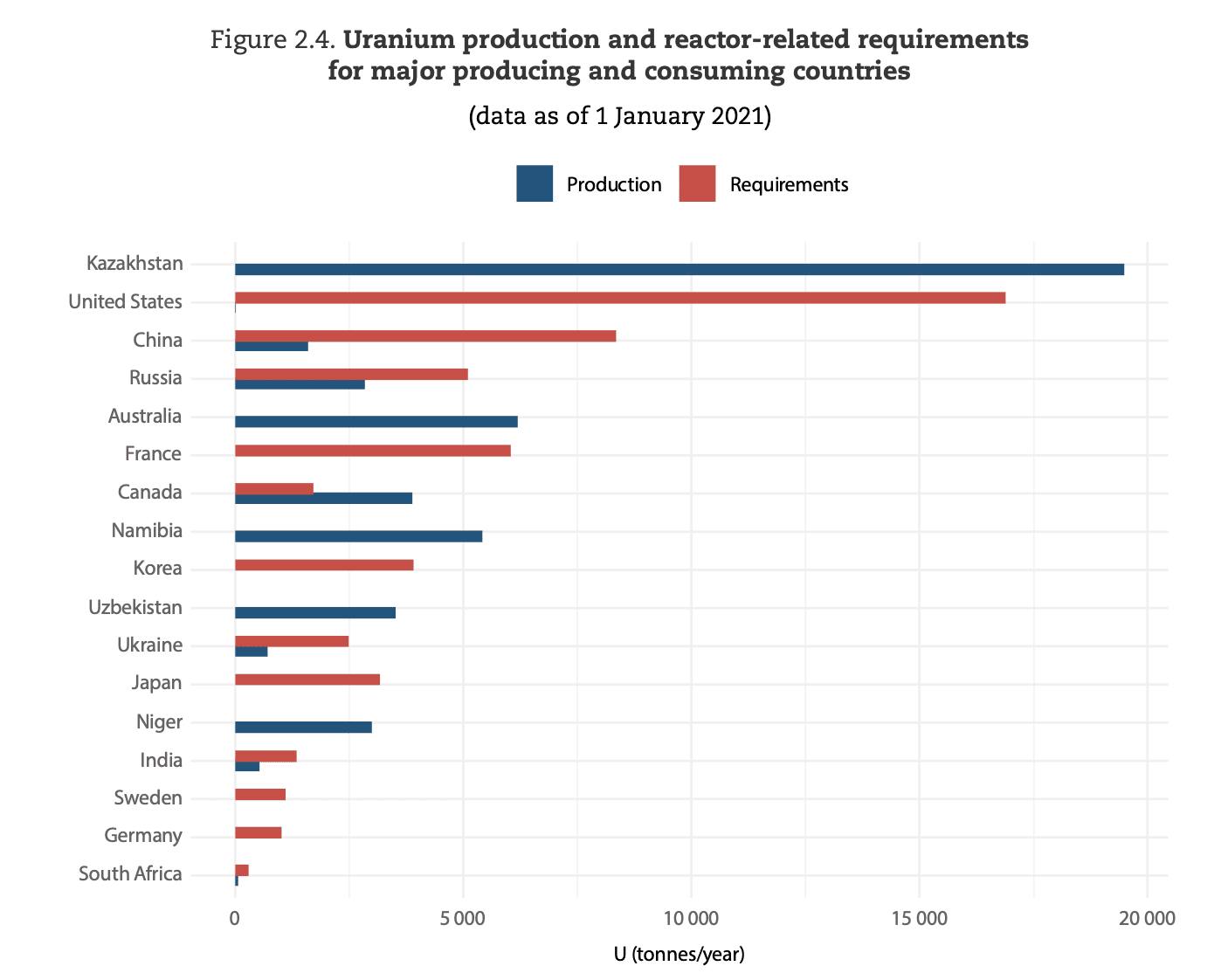

The U.S. is not alone in its need for uranium. We must notably see the American requirements in the light of the Chinese nuclear surge (see, “The Future of Uranium Demand – China’s Surge“). This is all the more important that the Chinese nuclear rise has started, whilst the American Renaissance remains an objective. In other words, China is already constructing new nuclear reactors and has already existing concrete plans for more nuclear plants. Hence its uranium requirements are firmer than those of the U.S.. Furthermore, China’s actions to supply its future uranium requirements have also already started. As a result, the options available to the U.S., and to other actors in terms of uranium supply, narrow down.

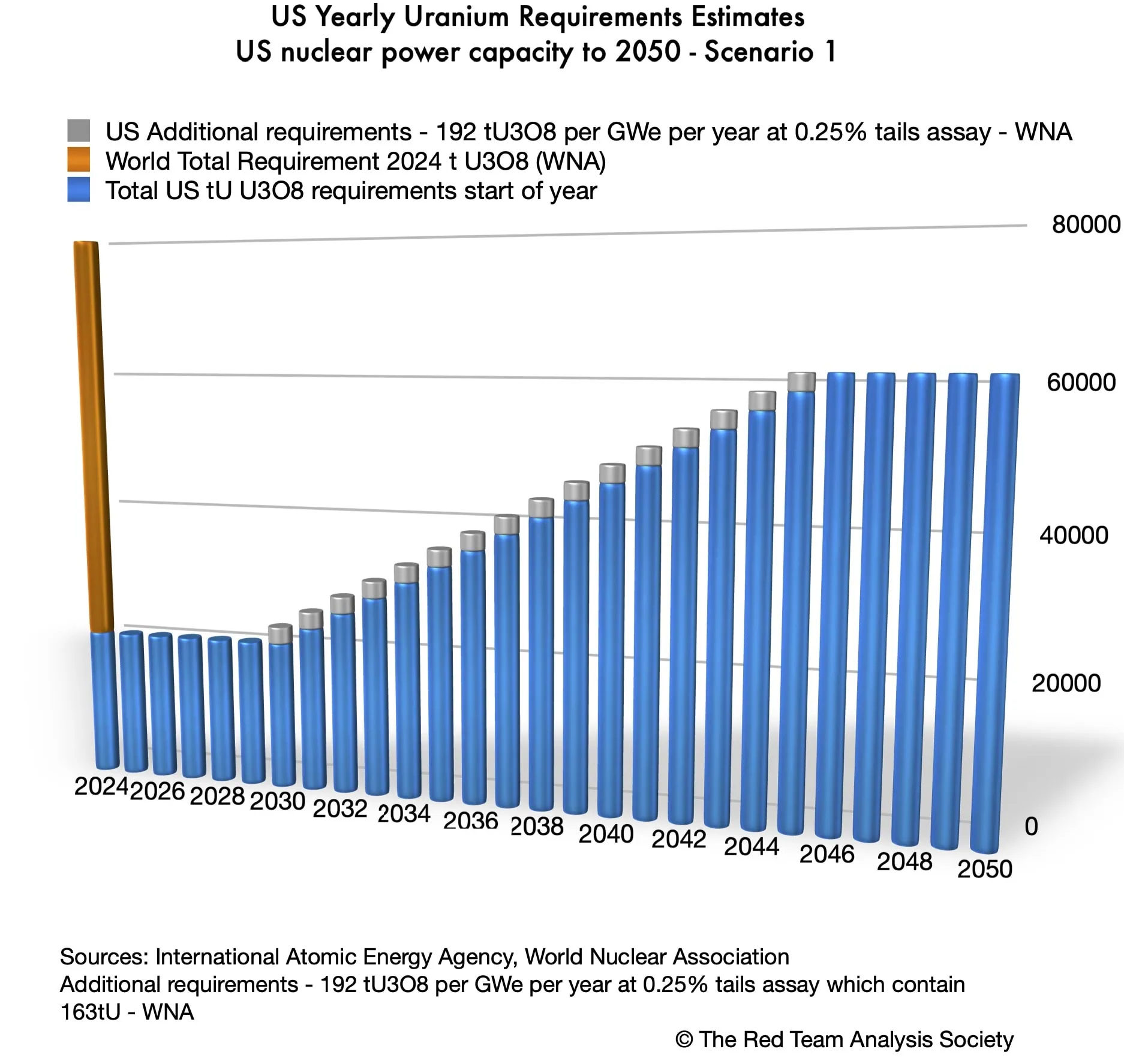

The American and Chinese requirements could look as shown on the two charts below.

U.S. and China yearly uranium requirements estimates 2024-2050

By 2044, American and Chinese yearly requirements will represent each approximately 80 % of 2024 global needs. For these two countries only, this amounts to almost 128.000 tU as U3O8, i.e. 1.6 times the 2024 requirements for the whole world.

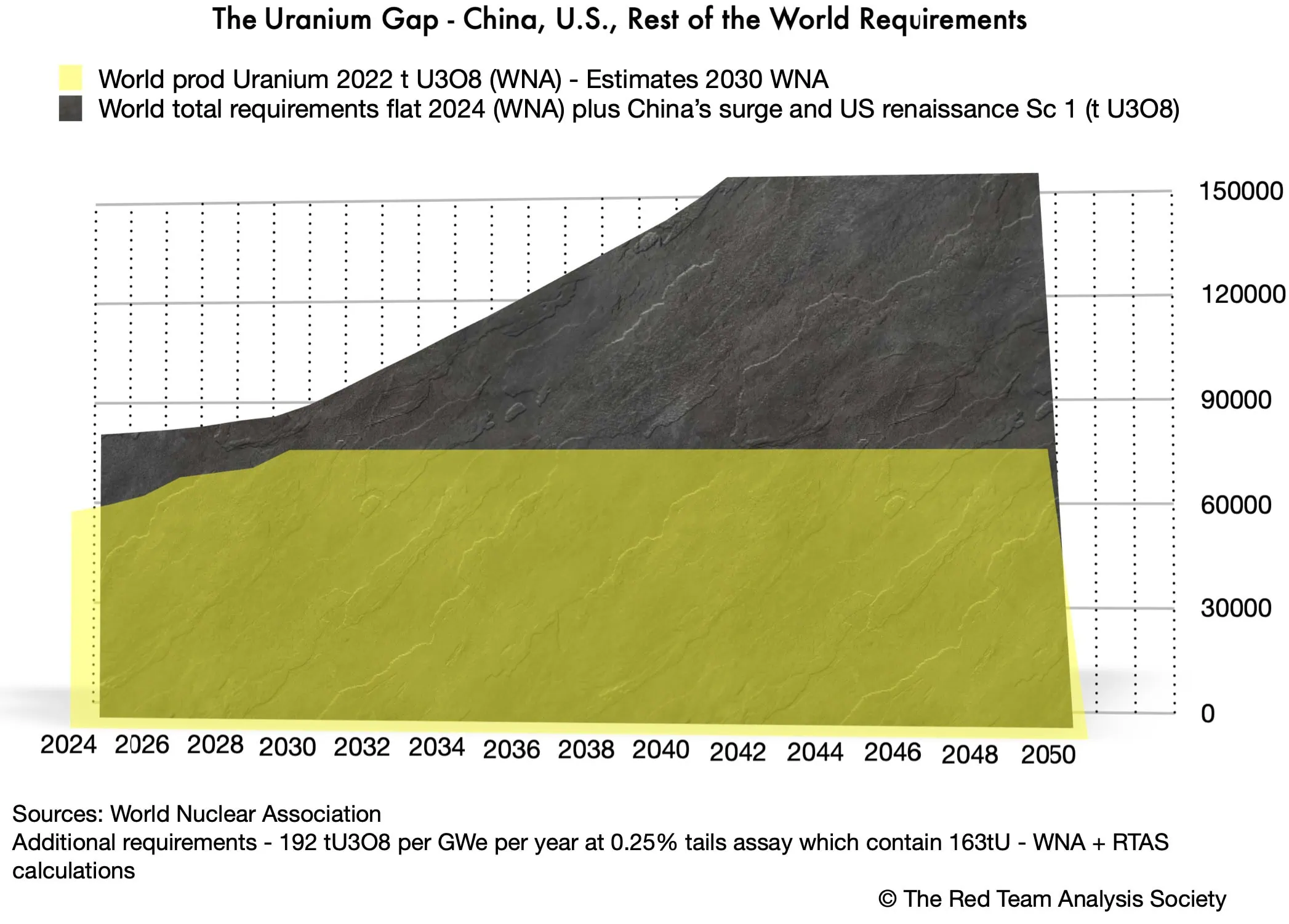

If we look now at uranium production (and not requirements), the World Nuclear Association estimates it reached 58,201 tU as U3O8 in 2022 (“World Uranium Mining Production“, 16 May 2024).

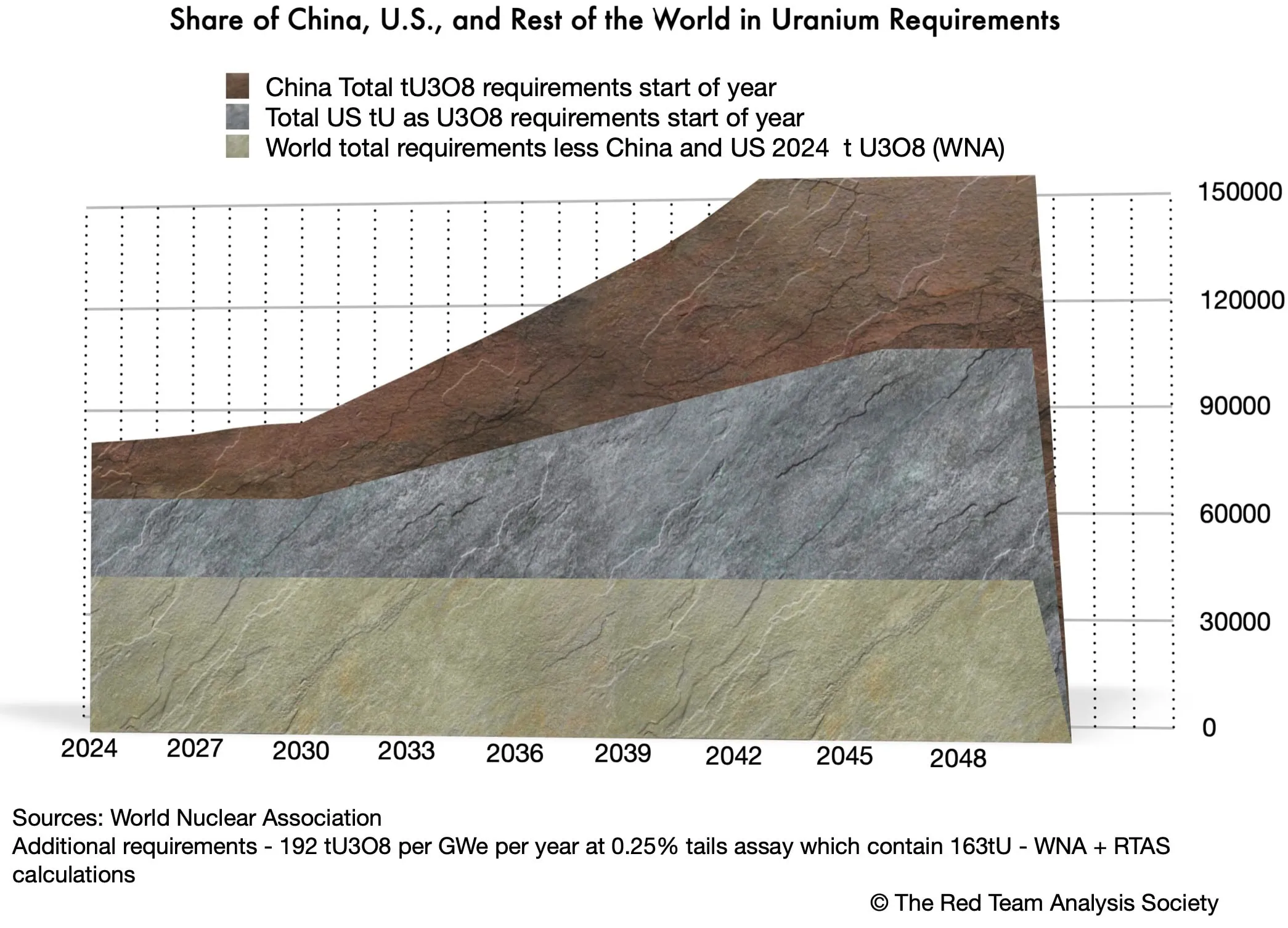

When we compare the Chinese and American uranium requirements plus the estimated amount required by the rest of the world – assuming for now this latter will not increase – with current production estimates, we obtain the following charts. The first one highlights in stone grey a rising global gap between the supply and demand of uranium, and the second the shares of the U.S. renaissance and of the Chinese surge in this rising gap.

The Uranium Supply and Demand Gap 2030-2050: American and Chinese Contributions

As in reality requirements for other countries will also very likely increase considering the global return of nuclear energy, and the willingness to treble nuclear energy worldwide, the gap between supply and demand is likely to be far worse than what is assessed here (Helene Lavoix, “The Return of Nuclear Energy“, The Red Team Analysis Society, 26 March 2024).

Global consequences of the uranium demand and supply rising gap

This rising global gap between supply and demand of uranium will have global impacts, which will then have consequences on each country according to its situation and actions in terms of nuclear energy and uranium supply. Those impacted will also be the U.S. and China.

The rising uranium global gap has three major consequences.

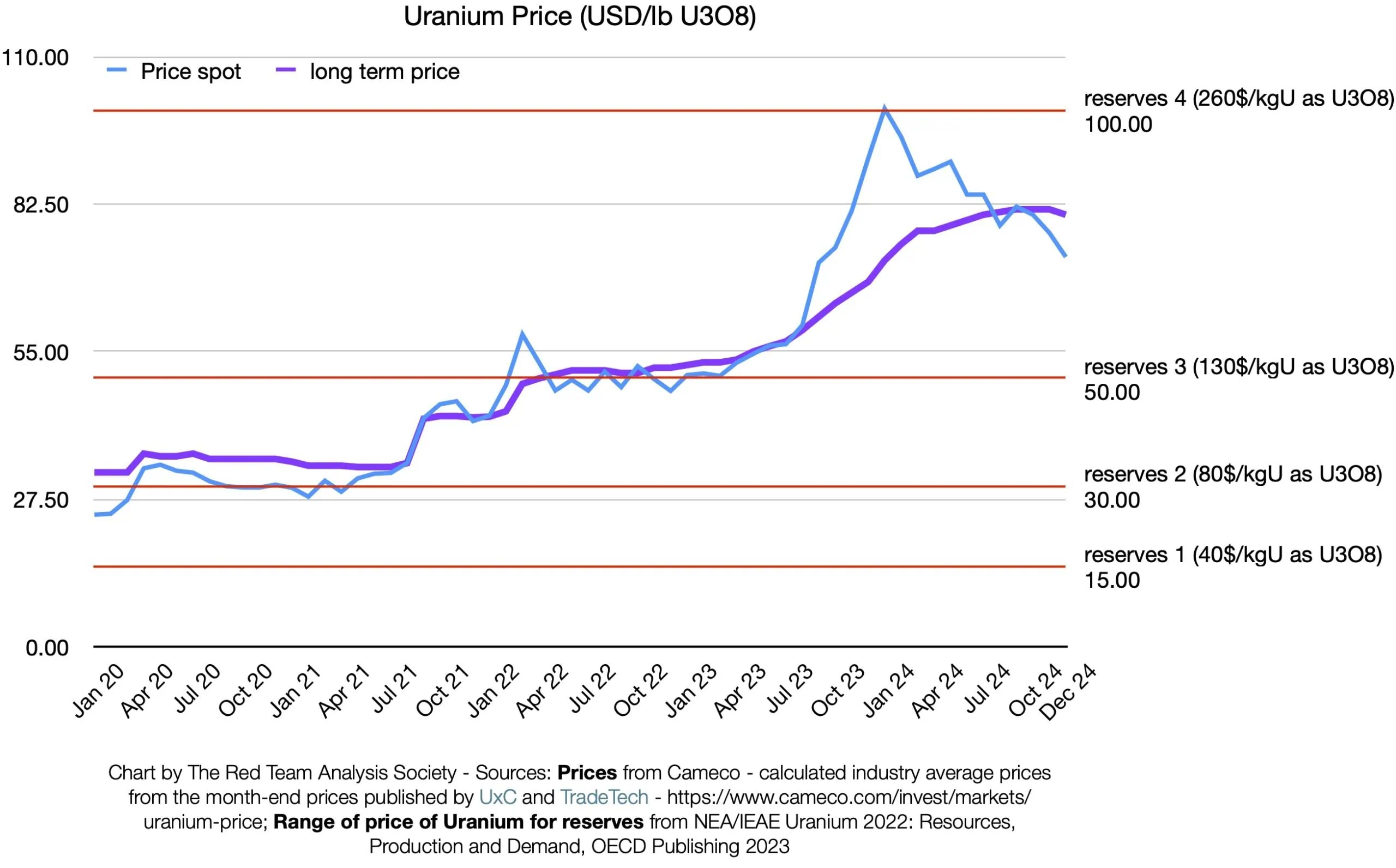

Rising uranium prices

Uranium prices will further increase, which will make new mines viable economically and allow for new production.

The slight decrease shown at the end of 2024 could result from a host of factors, from a divided EU regarding nuclear energy policy to a generalised temporary lack of awareness of the global supply demand gap, through wait-and-see behaviour considering the January 2025 change of Presidency in the U.S., from Biden to Trump (e.g. Kate Abnett, “New EU renewable energy target faces nuclear roadblock“, Reuters, 16 December 2024).

Uranium prices 2020-2024 spot market and long-term contracts.

As shown on the chart above, the NEA/IAEA Uranium 2022: Resources, Production and Demand (aka Red Book) uses various price ranges to evaluate reserves and resources in uranium (OECD Publishing, April 2023). The higher the price, the more reserves and resources of uranium available. We are steadily approaching the latest and highest price for the NEA/IAEA estimates of reserves and resources.

As the gap between supply and demand increases, prices will continue rising.

New mines and mills are imperative

New mines must be put into production and mills constructed, and this on a large scale considering future massive requirements notably from the U.S. and China. The mines with the largest reserves and resources will be sought first.

If mines and mills are not constructed on a large scale, then it is the entire “return of nuclear energy” that is endangered. Indeed, the security of uranium supply would then not be ensured, with consequences in terms of energy supply for countries relying on nuclear energy. As a result, the scenario Net Zero by 2050 for greenhouse gas (GHG) emissions would likely not be achieved, with negative feedback loops taking place (IEA, Net Zero by 2050 – A Roadmap for the Global Energy Sector, May 2021).

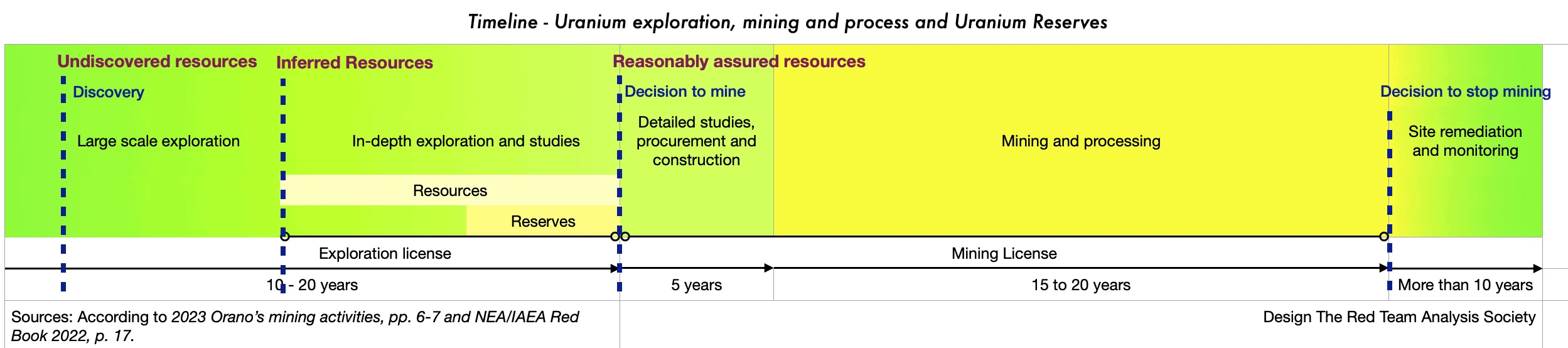

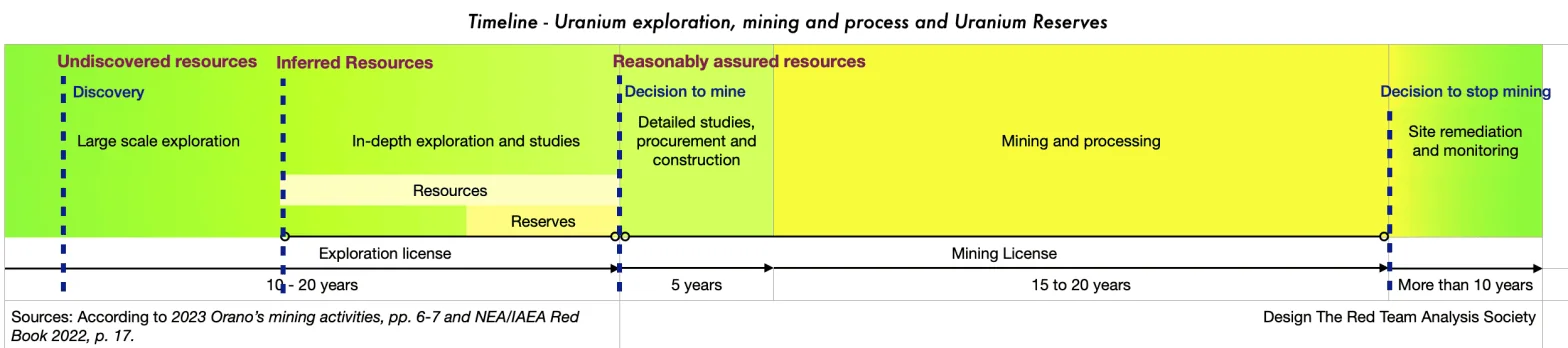

Considering the long timeline to bring a mine to production and the needed amount of financing, the uncertainty surrounding the American renaissance is rather bad news (for the uncertainty, see Towards a U.S. Nuclear Renaissance?).

Timeline – Uranium exploration, mining and process and Uranium Reserves

Indeed, if current mines waiting to be financed – and this is even worse for exploration projects – only find backers once those are almost certain of future requirements, i.e. at best, once a reactor has started being constructed and at worst once the timeline to completion of the reactor seems to be close to two years, then mining investment will likely come too late by three years in the worst case. To be too late by three years means that it will be impossible to start operating the new reactors as fuel will not be available. Nuclear plans will be delayed by at least those three years.

Even in the best case, risks remain. Mining investments will be done first by China and those countries that are considering the security of supply first and that benefit from state-led planning. In other words, when American and Western financiers will be ready to invest in mines because the construction of American reactors will have started, then they are likely to find out that the best mines with the largest reserves have already found financing and that their future production is already sold to others. If part of the production is still available for purchase, then, as ownership of the mining company will be in other hands, the security of supply for those future contracts becomes more fragile.

We can reason similarly for purchases of uranium through long-term contracts not involving investments in mining companies.

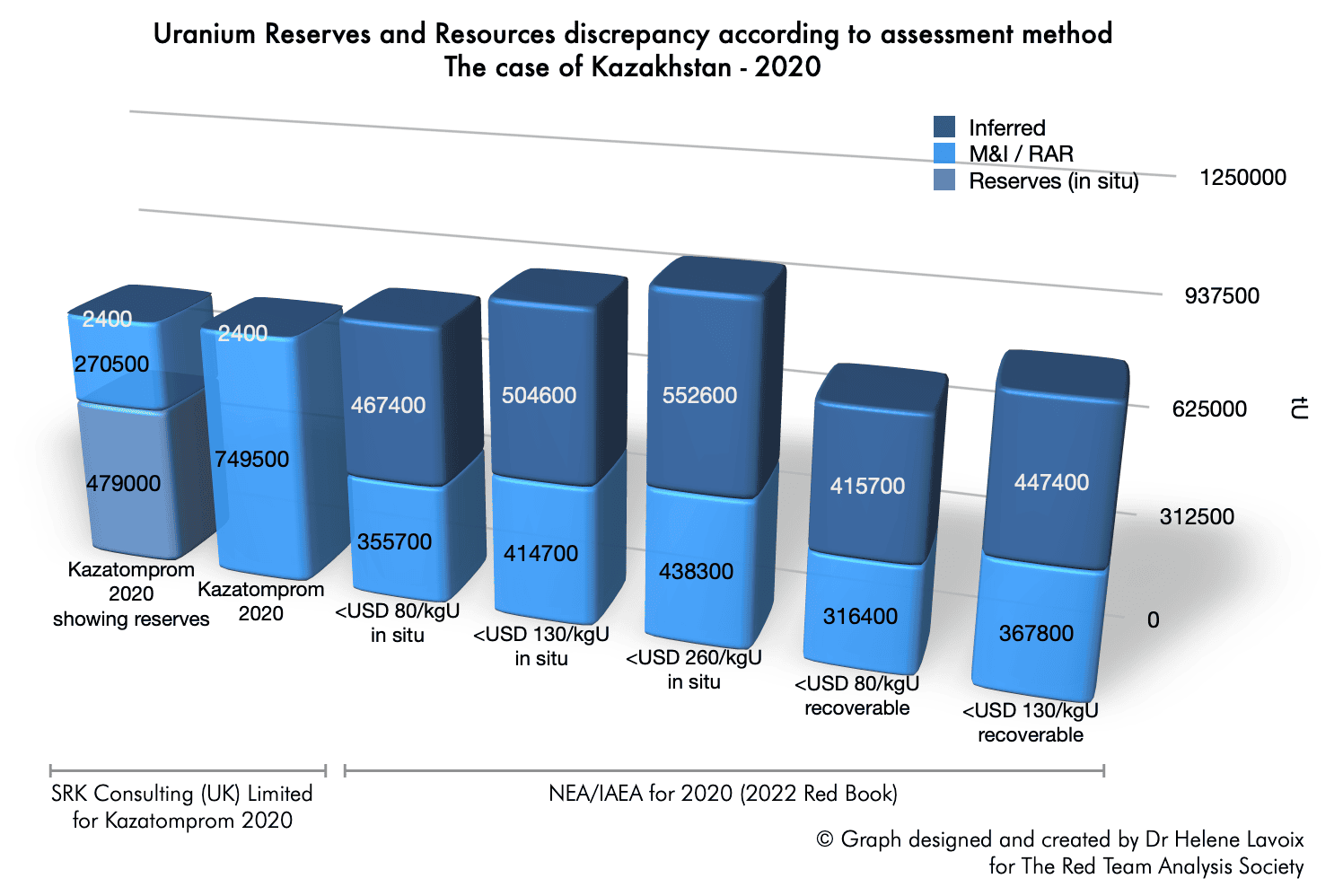

For example, on 15 October 2024, Kazatomprom (the national company of Kazakhstan, responsible for everything related to the nuclear industry) announced a 15 November extraordinary general assembly to vote on an agreement with CNNC Overseas Limited and China National Uranium Corporation Limited on the sale to the latter “of natural uranium concentrates in the form of U3O8 on market terms”. The assembly voted in favour of the agreement at 88.32% (15 Nov 2024 extraordinary general assembly).

The quantity of uranium for the agreement is not mentioned, but we may roughly estimate the overall Chinese purchases of Kazakh uranium, including this new agreement, to be at least between 11.800 and 14.977 tU as U3O8.(1) As the total Kazakh estimated production for 2024 could reach between 22.500 and 23.500 tU as U3O8, then the share already secured by China represents between 50% and 66.5% of the production in Kazakhstan, the first uranium producer in the world and the third most important country in terms of reserves (Kazatomprom 3Q24 Operations and Trading Update, 1 November 2024; chart “Revisiting Uranium Reserves and Resources : reserves, RAR and M&I resources” in Helene Lavoix, “Revisiting Uranium Supply Security (1)“, The Red team Analysis Society, 21 May 2024). If we look at the Kazakh production belonging to the country, which should reach between 15.500 and 16.500 tU as U3O8, it is between 71.5 % and 96.6% that could be bought by China.

China is thus already purchasing a very large amount of the uranium produced in Kazhakstan and an even larger amount of the Kazakh shares in this uranium. Hence, if future Chinese needs are to be satisfied, then new mines will imperatively have to be put into production. Indeed, Kazakhstan and Kazatomprom have an active policy of exploration and development of new mines (e.g. Kazatomprom News, “Kazatomprom obtains the right for uranium exploration at a new site of the Budenovskoye deposit“, 10 September 2024).

Now, we know that part of the Chinese purchases are spot and part are on the longer term (see fn 1). If the Chinese purchases, notably the long-term contracts, are on the “very” long term, for example ten years, then a probably large share of the 11.800 to 14.977 tU as U3O8 of Kazakh production cannot be anymore purchased by anyone else for those ten years. Thus, with the agreement accepted during the 15 November 2024 extraordinary general assembly, China would have secured enough uranium for approximately 78 GWe per year, whilst other countries, including the U.S., wouldn’t.

As a result, once ready to supply its new reactors, the U.S. will have to find other sources of uranium, assuming they are still available. Furthermore, as prices will go up, then the purchases the U.S. will be able to make will be more onerous.

As the whole world is de facto deprived of the Kazakh production bought by China, then it is not only the U.S. that needs to find other sources of uranium but the rest of the world too.

As long as a gap between supply and demand remains, each purchase of uranium and each investment in a uranium mining company and corresponding long-term supply contract rarefies the quantity of uranium that remains available to others. Hence competition for what is left will intensify.

Tough geopolitical competition for uranium

As a result, geopolitical competition to secure uranium supply will be tough.

Indeed, as stakes are high and as countries cannot afford not to have fuel available for their nuclear reactors, we can expect pitiless behaviour to obtain uranium (for stakes, Helene Lavoix, “Revisiting Uranium Supply Security (1)“, The Red Team Analysis Society, 21 May 2024).

The tension will be reinforced by belated financial decisions, besides an absence of awareness of the issue and a related lack of anticipation (see Uranium and the Renewal of Nuclear Energy).

The excellent relations and strategic partnership existing between Russia and China plays to their advantage.

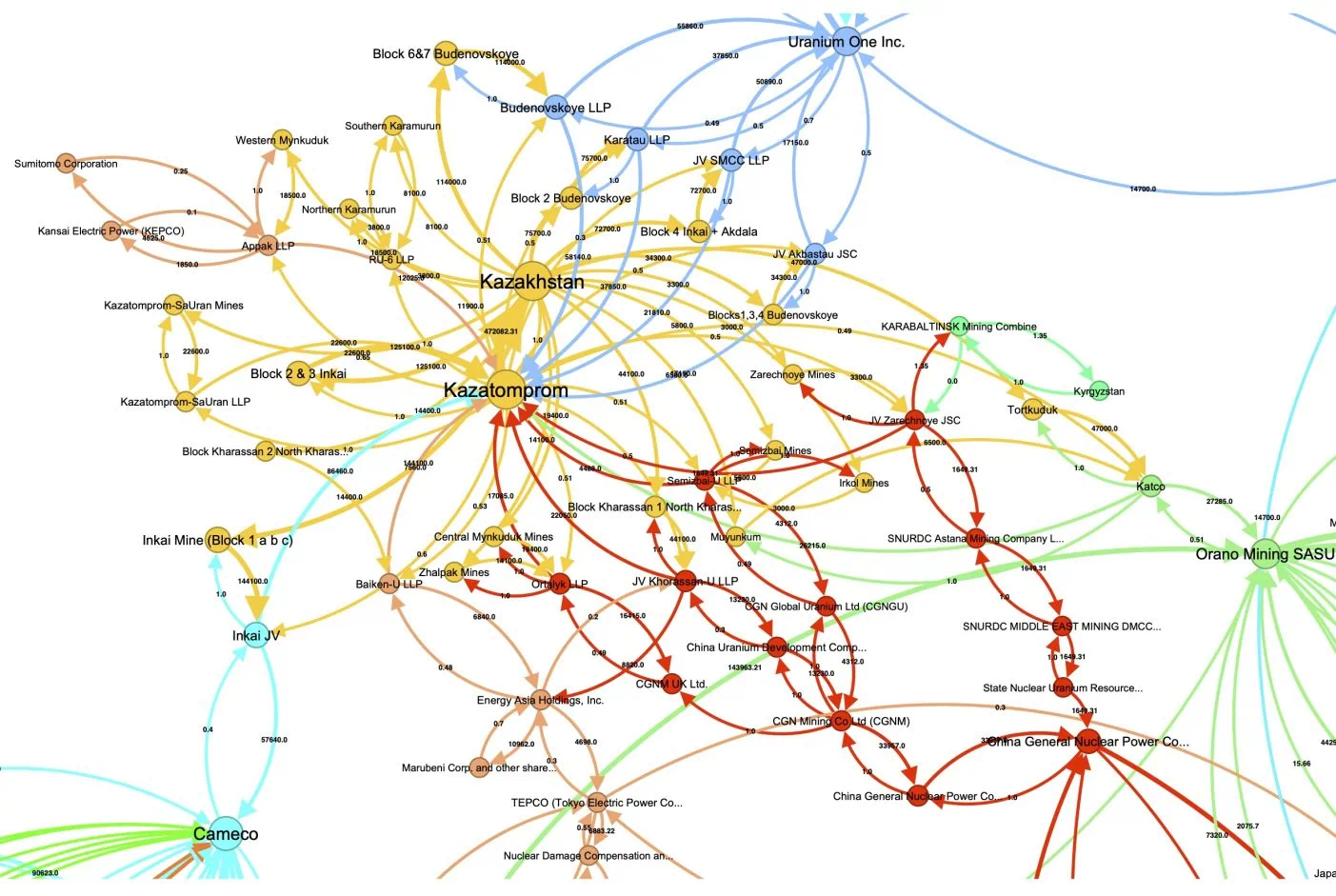

For example, on 17 December 2024, Kazatomprom announced changes of partnership in some of its joint ventures. Russia sold the whole of its shares (49.979%) in JV Zarechnoye JSC to China and is expected to sell 30% participation interest in the capital of JV Khorasan-U LLP (mining) and 30% participation interest in the capital of Kyzylkum LLP (uranium processing facilities) also to China (Kazatomprom News, “Kazatomprom announces the change of the partners in some JVs“, 17 December 2024).

As a result, the new shares of Kazakh reserves and measured and indicated resources in uranium, as well as the related web of stakes looks as on the graph on the right hand side.

In terms of reserves and resources, Russia thus has ceded to China 1.649 tU as U3O8 for JV Zarechnoye JSC (end of life of mine 2028) and 13.230 tU as U3O8 for JV Khorasan-U LLP (end of life of mine 2038).

Mines, Reserves and Resources, Joint Ventures and shareholders in Kazhakstan – after the sino-russian deals and exchanges – December 2024 [ Kazakhstan: yellow, Russia: powder blue, China: red; France: light green, Canada: turquoise, Japan: beige, Kyrgystan: green) – Created with The World of Uranium 2

Those who will be too late in waking up to the new geopolitical competition for uranium may well start buying candles and think about forced de-growth. Alternatively, wars and special operations aiming at securing uranium may become necessary.

Ways forward for the U.S.

Against this highly volatile and challenging backdrop, what are the options opened to the U.S.? The question is of interest not only to the U.S. but also to all other players in the nuclear energy field, considering the global quality of the sector and the weight of the U.S. requirements, should the country manage to go ahead with its plans for nuclear energy.

Relying solely on the invisible hand of the market?

As seen, in 2023, in the U.S., only 4,65% of the uranium delivered originated from the U.S., i.e. came from American deposits, whilst 95,35% came for foreign countries (see Uranium for the U.S. Nuclear Renaissance…). Only 3.88% of the uranium delivered to the United States was purchased by American suppliers, whilst 96.12% was purchased by foreign suppliers (Ibid.).

For the future, the U.S. could thus hope to rely on a similar system, imagining that, as its uranium requirements increase, the market will “automatically” adjust and supply the quantity of uranium needed.

However, this assumes that the private sector from “allies and partners”, to use the U.S. Department of Energy words, will accept to take the risks linked to the supply of uranium, for example those related to delays in terms of nuclear reactors’ construction and corresponding skyrocketing costs (2024 Pathways to Commercial Liftoff: Advanced Nuclear, p.57; for the risks, see “Towards a U.S. Nuclear Renaissance?“). To offset or to the least mitigate those risks, it is likely that companies will tend to be too late in their mining investments rather than too early.

Furthermore, companies will also have to serve all their clients, not only the U.S.. They may thus very well decide to split supplementary production between clients, leaving the U.S. short on its uranium needs. As those companies are not, for the most part, American companies, the U.S. may have little means to pressure those companies for priority supply, in market conditions.

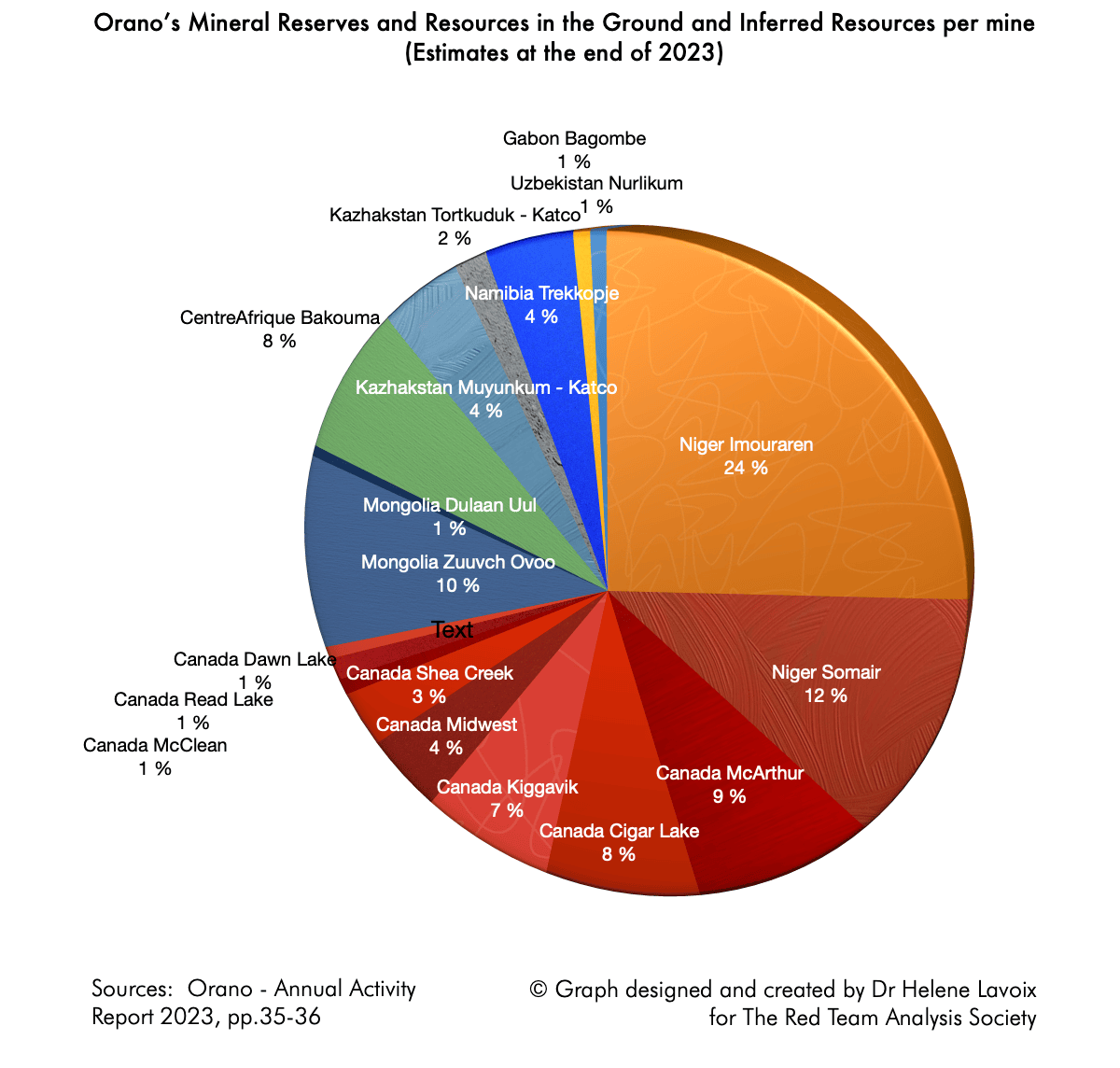

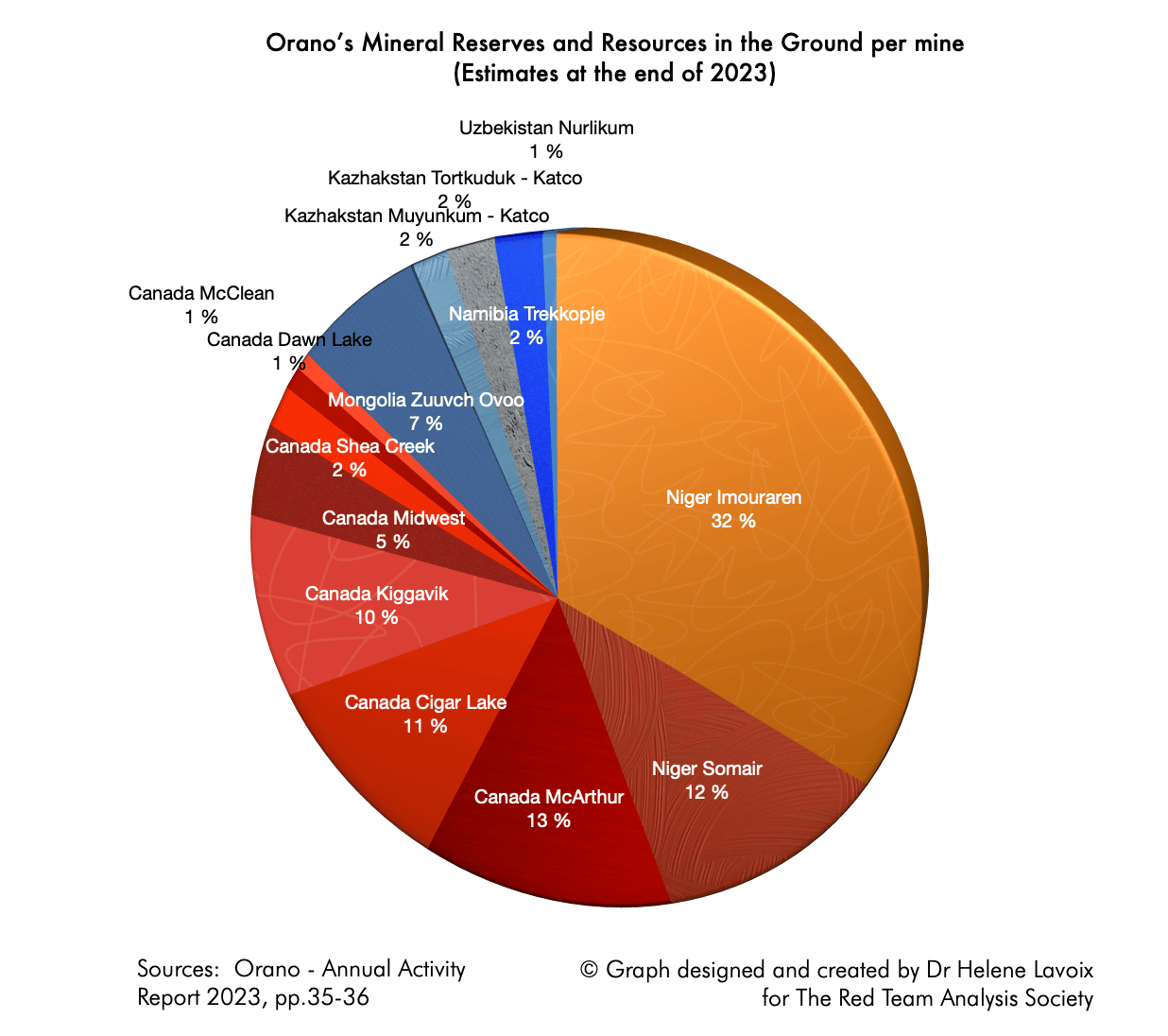

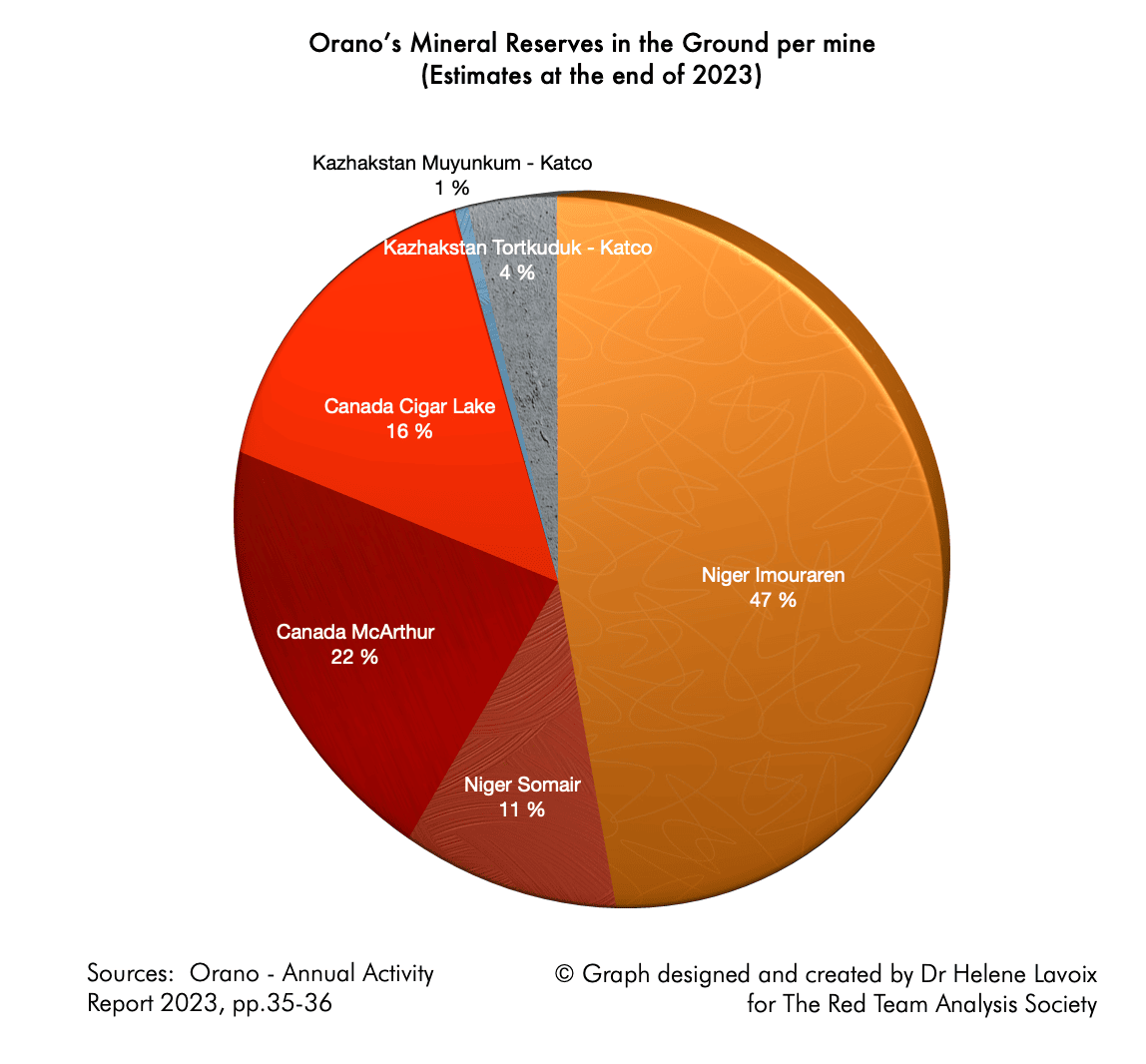

Finally, some of the companies supplying the U.S. are state companies, such as Orano. What does that imply?

Let us go back to the assumption made in the previous article, according to which the increase in production planned by Cameco and French public company Orano for their plants of Cigar Lake(2)and McArthur River/Key Lake(3) is meant to cover the American uranium requirements consequent to the loss of the Russian and Nigerien uranium supply. Previously we imagined that Cameco and Orano would sold all the supplementary uranium produced to the U.S..

Yet, other hypotheses are possible.

If the EU were following the U.S. and sanctioning Russian uranium, or if ever Russia were to decide to ban uranium exports to Europe, then European states would have to find elsewhere corresponding uranium requirements, as well as new ones (EU Parlement, Parliamentary question – E-001721/2024 and answer; Gabriel Gavin and Victor Jack, “EU eyes new clampdown on Russian nuclear sector“, Politico, 5 November 2024). This would be added to the loss of Niger’s uranium (Niger: a New Severe Threat for the Future of France’s Nuclear Energy?). France notably, with its very high stake in nuclear electricity, would be challenged to find a much needed uranium (Revisiting Uranium Supply Security – 1). True enough, Orano progresses in finding new uranium supply sources, for example in Mongolia (e.g. “Mongolia and Orano sign pact for first ever ‘Mongolia-France’ uranium project, International Mining“, 28 Dec 2024). Yet, for that project, production will start in 2028, and peak in 2044 at 2.600 t, 10% of the production being reserved for Mongolia (Ibid.). Compared with the loss of Niger (i.e. France’s share which amounts to 1.268 tU per year), at peak, Orano will thus see its production increase by 1.072 t. It will nonetheless have to find uranium until 2028 to honour its contracts and for France needs. Assuming French uranium stocks are not used, France could be forced to keep any increase in uranium production for its own needs until the Mongolian production starts (Revisiting Uranium Supply Security – 1).

Furthermore, tension between France and Azerbaijan, a key country of the Trans-Caspian International Transport route also known as the Middle Corridor, could also complicate French uranium supply from Central and Eastern Asia (Dauren Moldakhmetov, “What Does the Future Hold for the Middle Corridor?“, The Times of Central Asia, 31 July 2024; among others, R.D. avec AFP, “Tensions France-Azerbaïdjan : la charge d’Ilham Aliev contre le “régime Macron en Outre-mer“, L’Express, 13 November 2024). Assuming this is possible, considering notably the remaining part of the uranium fuel cycle – conversion and enrichment – we may imagine French Orano could have to route Central and Eastern Asian uranium to its Asian clients, rather than using the very long maritime route through a Chinese port, the strait of Malacca and the cap of Good Hope, if the Houthis continue to endanger the Suez Canal route, to bring Asian uranium to Europe.(4) In that case, it could decide to use Canadian uranium for France’s needs, as well as for its non-Asian and European clients. Swaps and barter between companies can also be imagined.

As a result of these potential challenges, as French Orano holds shares in the two Canadian mills of Cigar Lakeand McArthur River/Key Lake, assuming contracts allow it, France could decide to keep its part of the increase, i.e. 740 tU as U3O8. In that case, the U.S. would have to find elsewhere 740 tU as U3O8 on a yearly basis.

What we see here emerging with this example – even if it is hypothetical – is that geopolitical decisions (sanctions) and tensions have impact on uranium supply and that stakes in uranium supply may in turn impact decisions regarding uranium that will in turn have geopolitical consequences.

Furthermore, this example also shows that decisions cannot be taken at a macro level but must consider the situation of each country and of each mine and mill.

If we consider the three points above – the risk of uranium supply born mainly by private companies, the imperative, for overseas private companies, to serve all clients, and the uncertainty stemming from using foreign states companies when those states have stakes in nuclear energy – we find that it may prove insecure for the U.S., and actually for all countries, to rely primarily or solely on companies, and worse still on foreign companies, for their uranium supply.

The U.S. DOE’s idea according to which “Mining/milling of uranium will need to be increased from the US, allies, and partners to ensure a secure supply” may very well become impossible, considering geopolitical tension, the uranium supply -demand gap to which the U.S. largely contributes besides China and the needs of these allies and partners (Ibid. p.57).

Actually, the more the global race for uranium intensifies, the less relying exclusively on the invisible hand of the market will ensure a secure supply.

Emulating China’s three pronged uranium policy

The disinterest in terms of production and purchase of uranium by U.S. companies is not only a disadvantage considering the U.S. nuclear renaissance’s objectives, but also a security liability, considering the various stakes of this renaissance, if remedies are not designed (see Towards a U.S. Nuclear Renaissance?).

The Chinese uranium supply policy to rely for one-third on domestic production, for one-third on overseas production through equity and joint ventures and for one-third on purchases cannot be applied as such and at once to the U.S. considering the size of the American resources and reserves and the disinterest of American companies in overseas uranium mining (for the Chinese policy, WNA, “China’s Nuclear Fuel Cycle“, 25 April 2024). It could however be progressively emulated with as objective for 2050 to increase production domestically as much as possible, and for the remaining part of the requirements to rely on purchases for half of the needs and on overseas production though equity and joint ventures for the other half.

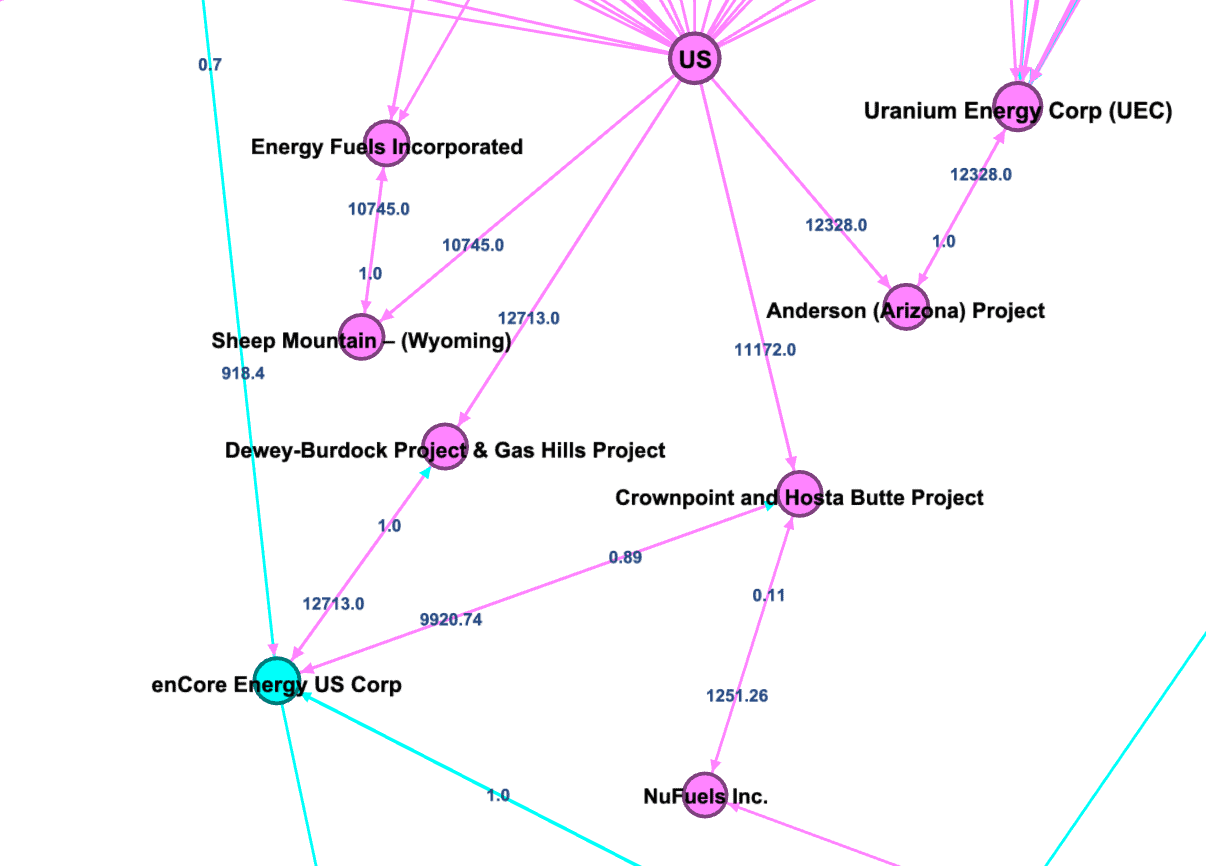

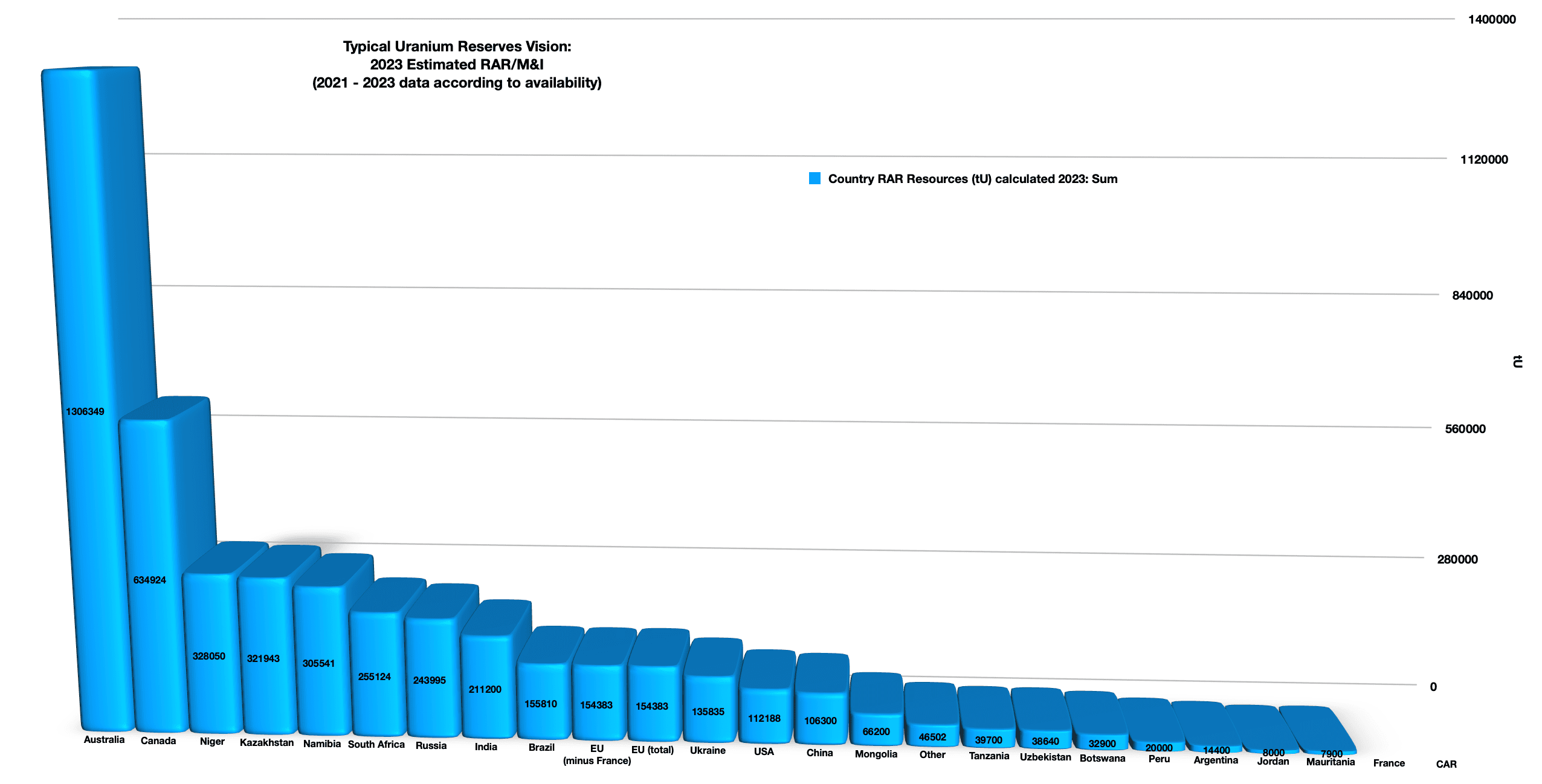

Even though reserves and resources are smaller in the U.S. than in many other countries, they reach nonetheless 147.820 tU as U3O8, when adding all the assessed mines and deposits (see The World of Uranium – 1: Mines, States and Companies – Database and Interactive Graph; “Uranium for the U.S. Nuclear Renaissance…“). Assuming the mines and deposits are truly economically viable, and can be developed considering environmental constraints and indigenous peoples’ rights, the American mines with the largest reserves and resources could be chosen for priority development and thus financing.

For example, the following deposits could be selected: the Anderson project in Arizona belonging to U.S. Uranium Energy Corp (UEC), Sheep Mountain in Wyoming belonging to U.S. Energy Fuels Inc., the Dewey-Burdock Project & Gas Hills Project of Canadian held enCore Energy US Corp and the Crownpoint and Hosta Butte Project belonging to the same company and to Nufuels Inc. (identified through The World of Uranium – 2)

Then, U.S. mining companies, which are solid enough financially to do so, could attempt to take hold or create joint ventures with current holders of large foreign deposits close by, i.e. in Canadian Saskatchewan. Alternatively, concerned actors such as U.S. specialised funds could finance mines in a way that would include an agreement to preempt production for U.S. purchase.

The Rook 1 Project of NexGen Energy Ltd with its 98.738 tU as U3O8 reserves and resources is an obvious candidate. According to NexGen Energy Ltd plans, the mine would produce approximately 11.232 tU as U3O8 per year (29.2 Mlbs U3O8 per year for the first 5 years, with possible expansion from year 6 to end of mine life (11.7 years) – NexGen Investors presentation December 2024). For 4.5 years, the U.S. would have enough uranium for its supplementary requirements. However, after that time, it would again have to find new mines. It would also have to make sure that production of the Rook 1 project does not decrease after the initial 5 years.

If we consider the option to invest as much as possible in mining companies in Saskatchewan, how much of the uranium of Saskatchewan could be needed for the American nuclear renaissance?

The current estimates for the main reserves and resources known for Canadian Saskatchewan (Ca) amount to 555.258 tU as U3O8 (The World Of Uranium-1 and 2). If we remove the two largest mines already exploited, Cigar Lake and McArthur, the remaining amount of reserves and resources amounts to 315.584 tU as U3O8 (The World Of Uranium – 2). We saw the U.S. requirements for scenario 1 of the nuclear renaissance corresponded to an increase of 2.496 tU as U3O8 per year in terms of supply, starting in 2029-2030, to reach from 2045-2046 61.324 tU as U3O8 of yearly requirements. Thus, if we assume that all reserves and resources of Saskatchewan are used exclusively for U.S. requirement needs, then during the year 2045, all the known uranium in the Canadian province will have been used.

This hypothesis is unlikely considering that the main companies operating in Saskatchewan are Cameco, a private global Canadian company with clients worldwide, and French Orano also with clients worldwide and the need to serve in priority France with its high stake in nuclear energy.

Thus U.S. companies will not only have to invest as much possible in Saskatchewan, considering other states’s needs, but also in other Canadian provinces such as the Nunavut and Labrador and fundamentally everywhere in the world where uranium can be mined.

Furthermore, an intense exploration policy for uranium mining will need to be carried out as soon as possible considering high uncertainty and long timeline, as shown by the hypothesis of an exclusive American use of all Saskatchewan reserves and resources. Without exploration, if the U.S. nuclear renaissance takes off, it will be impossible to meet the requirement needs of the U.S. and of other countries by the end of the period.

This could also mean an even more intense geopolitical competition.

Ensuring territories endowed with uranium supply the U.S. first?

Considering the stakes, and faced with the imperative of uranium supply security, in a highly competitive geopolitical environment, the U.S. may choose to annex, one way or another, territories endowed with uranium resources, besides other critical minerals and other strategic assets.

We find here a logic to U.S. president-elect Trump’s declarations regarding his desire to make Canada an American State and to buy Greenland, which uranium potential is “considered [as] relatively high”, according to the 2018 Official Geological Survey Uranium potential in Greenland (e.g. Jessica Murphy, “Trudeau says ‘not a snowball’s chance in hell’ Canada will join US“, BBC, 7 December 2025; Maia Davies, “Greenland ready to work with US on defence, says PM“, BBC, 13 January 2025). The Republicans’ attempt to introduce a bill in the House of Representatives (the “Make Greenland Great Again Act”), which would allow the U.S. to buy Greenland, underlines the reality and seriousness of President Trump’s proposal (Magnus Lund Nielsen, “Make Greenland Great Again Act seeks support in US“, Euractiv, 14 January 2025).

The U.S. would thus start a whole new period for international politics, one where the principles built from the Montevideo Convention on Rights and Duties of States (1933), and then enshrined in the United Nations charter, signed on 26 June 1945, in San Francisco, have become outdated. We would be back to a time where conquest and war become fully part again of international relations.

If ever the U.S. were really annexing Greenland or any other territory, then the security of its uranium supply would be greatly enhanced for the amount of uranium held by the territory annexed. However, here, this uranium would not anymore be available to others. As China will also have secured, in a different way the uranium it needs, the remaining uranium would have shrank drastically. This is not anymore a couple of mines or part of a production that would be removed from the market, but a whole territory endowed with many mines and deposits. According to their stakes in nuclear energy, and to their power, other states would then have to compete for what is left. The likelihood to see force being used is greatly heightened.

Even if war does not ensue from Trump’s declaration and if the “Greenland Act” is not voted, current reactions from Greenland and Denmark to the threats nonetheless seek to appease the U.S. by giving it more than it had before, while also stressing the sovereignty of Greenland (e.g. Davies, “Greenland ready to work with US on defence, says PM“, BBC, 13 January 2025). As a result, by making concessions, Greenland and Denmark tend to condone the change of principles.

Thus, geopolitical race and tensions for uranium supply security could very well be not only an instance of forthcoming wars for resources, but also participate in signalling and spearheading a very change of the international order.

Notes

(1) Estimating roughly the amount in t U as U3O8 of the agreement between Kazatomprom and CNNC Overseas Limited and China National Uranium Corporation: We know that “The transaction value, cumulative with the previously concluded transactions with CNUC [long-term contract] and CNNC Overseas [spot], comprises fifty percent or more of the total book value of the Company’s assets”, hence Kazatomprom extraordinary general assembly. The total asset of Kazatomprom was 3.331.448 million KZT on 30 Sept 2024 (Kazatomprom consolidated statements p.12). Thus, the total amount of sales of uranium concentrate to China, including prior contracts, could be over 1.665.724 million KZT after the EGA on 15 November 2024, i.e. approximately 3.173.32 million USD. We also find sources giving the amount of $2.5 billion USD (e.g. Olga Tonkonog, “Kazakhstan to finalize major uranium deal with China“, Kursiv, 15 October 2024; Vagit Ismailov, “Chinese Companies to Purchase Uranium Concentrates from Kazatomprom for $2.5 Billion“, The Times of Central Asia, 18 Nov 2024).

If we assume an agreement using September 2024’s long term uranium price, i.e. USD 81,50/lbs U3O8 (Cameco), then the minimum quantity purchased as a whole by China to Kazakhstan could be 38,937 Million lbsU3O8, or 14.977 tU as U3O8. The quantity could be larger as previous contracts were certainly contracted at a lower price. If we take the figure of 2.5 billion USD, then the global purchase of uranium concentrate by China could be 11.800 tU as U3O8. These amounts are only very rough estimates, given the number of assumptions made.

The total amount of sales to China was 540.405 million KZT on 30 Sept 2024 (against 342.293 million KZT in Sept 2023 and 522.521 million KZT on 31 Dec 23, Ibid. p.13 and Notes to the Consolidated Financial Statements – 31 December 2023, p. 15). This shows a consequent increase in Chinese purchases has already taken place.

(2) Cigar Lake is owned at 54.547% by Cameco, 40.453% by Orano Canada Inc. (Orano) and 5% by TEPCO Resources Inc.

(3) The Key Lake mill is owned 83.333% by Cameco and 16.667% by Orano.

(4) Estimated transit times

Shipments from major Chinese ports to North America’s West Coast ports

Russia, India, Japan, China, the United Arab Emirates, the U.S., the European Space agency, etc. are all sending robots on the Moon or on Mars. On 26 September 2022, the U.S. NASA purposefully projected a spacecraft on asteroid Dimorphos. Such was the precision and the force of the impact that it opened a crater in the middle of the asteroid, while altering its trajectory (Keith Cooper, “NASA’s DART mission hammered asteroid Dimorphos into a new shape. Here is how“, Space.com, March 21, 2024).

Those countries and international organizations are all developing ways and means to materially intervene on space bodies.

Indeed, those minerals are essential to the material foundation of the current worldwide energy transition including the related nuclear renaissance, to the exponential development of AI and its militarization and of the digital economy, to the development of urban life, and to the rapid development of Asian countries ( “EXECUTIVE SUMMARY – In the transition to clean energy, critical minerals bring new challenges to energy security“, International Energy Agency / IEA, March 2022).

Thus, it is not surprising that mines, ore deposits and geological prospects are, one way or another, increasingly important in current conflicts, wars and geopolitical realignments.

For example, one can note that several african, asian and south-american countries are members of the Chinese Belt&Road, knowing that the purpose of this Chinese grand strategy is to bring resources in China (Jean-Michel Valantin, “China and the New Silk Road: From Oil Wells to the Moon… and Beyond “, The Red Team Analysis, 6 July, 2015).

However, the relentlessly mounting pressure on geological resources puts the current global development dynamic on a collision course with the geological “limits to growth” (Gaya Herrington, “Update to Limits to Growth, Comparing the World 3 model to empirical data“, KPMG LLP, Stanford University,2020).

In this context of progressively depleting mineral resources, space bodies are more and more attractive, because they are rich with “high concentrations of rare metals—platinum and gold for electronics, nickel and cobalt for catalyst and fuel-cell technology, and, of course, iron” (Bertrand Dano in Robert C. Jones Jr, “The New space race: mining for minerals on asteroids“, News@TheU, Ubniversity of Miami,, 10/09/2024)..

Reaching those deposits, mining them and bringing them back to Earth necessitates to reinforce robotics, space technology dimensions of artificial intelligence (Jean-Michel Valantin, “Space mining, Artificial intelligence and transition“, The Red Team Analysis Society, March 19, 2018).

Indeed, lunar and asteroid landers and robotic miners will have to be strongly autonomous. Thus, the race to space mining entails immense technological challenges and financial hurdles. And yet, it is taking place.

If we adopt a geopolitical look, it appears that the race for space mining is happening between two large “geopolitical partnerships”, i.e “the West” on the one hand and “the BRICS” on the other.

The original BRICS are the group composed of Brazil, India, Russia, China and South Africa.

In 2023, the group integrated Egypt, Iran, Ethiopia and the United Arab Emirates, while Saudi Arabia is still considering the invitation (Fyodor Lukyanov et al., ” The BRICS Summit 2024: an expanding Alternative“, Council on Foreign Affairs and the Council of councils, 7 Novembre, 2024).

BRICS members, as well as the U.S. and the European Union, are developing space mining projects and strategies. Thus, this race projects the current strategic competitions between western countries and BRICS countries in outer space. Hence, the race to space mining becomes the “continuation of geopolitics through space means”.

We are going to study which of the BRICS countries join the space mining race. Then we shall see how this race is intricately linked with the development of artificial intelligence. Then, we shall highlight that this race is also a geopolitical one, and as such a potential preparation for (not so) future realignments.

The Moon south pole attracts this new wave of robotic exploration because it may contain water in craters. This lunar region is highly exposed to the sun. Thus, lunar robots may use both sun energy and water in order to build permanent bases (Guy Faulconridge, “Explainer: Moon mining – Why major powers are eyeing a lunar gold rush ?”, Reuters, August 11, 2023. Those landers and robots benefit from the exponential progress of AI machine learning (Ayaan Naha, “How rovers use machine learning to navigate Mars and the Moon?“, Medium, October 12, 2023).

To be or not to be on Mars

As it happens, two U.S. rovers and one robot helicopter, a United Arab Emirates rover and a Chinese rover are already exploring the surface of Mars. Russia, India, the European Union and the U.S. are preparing new Mars missions. If the U.S. and the EU have already launched human beings in space and on the Moon, some of the BRICS – Russia, China and the UAE – are also space faring countries.

Some of the prominent members of the BRICS, such as Russia, are openly expressing their space mining intent and goals. After the August 2023 Moon landing failure of a Russian space craft, Boris Yusimov, Roskosmos chief declared:

« This is not just about the prestige of the country and the achievement of some geopolitical goals. This is about ensuring defensive capabilities and achieving technological sovereignty … Today it is also of a practical value because, of course, the race for the development of the natural resources of the moon has begun. And in the future, the Moon will become a platform for deep space exploration, an ideal platform. » (“Race for Moon resources has begun, says Russian Space chief after failed lunar mission“, Reuters, August, 2023).

China on the Moon

China, the other main driver of the BRICS with Russia, is also laying plans to mine the Moon and asteroids. Indeed, in 2023, the Chinese government submitted a proposal at the UN working group on the Peaceful uses of outer space. The Chinese document aims at establishing the legality of space resources exploitation, respecting the framework of the 1967 Outer Space Treaty. Thus, China proposes to exploit space resources without national annexations of the Moon or other celestial bodies (Andrew Jones, “China outlines position on use of space resources“, Space News, March 6, 2024.

Meanwhile, in May 2024, the Chinese Space Agency launched the Chang’e 6 mission. At this occasion, a lunar rover took samples of the Moon surface. Those were brought back on Earth on 25 June 2024. This mission precedes the Chang’e 7 and 8 missions that should take place respectively in 2026 and 2028. Those missions will explore the availability of Moon resources as well as the Moon South pole (Andrew Jones, “China Chang’e 7 mission to targer Shackleton crater”, Space News, 30 January, 2024).

They will be instrumental for establishing the technological conditions for a permanent Lunar robotic and inhabited base, around 2030, the International Lunar Research Station (ILRS). This project already involves Russia, as well as numerous other countries. Among them are Venezuela, Belarus, Pakistan, Azerbaijan, South Africa, Egypt, Nicaragua, Thailand, Serbia ad Kazakhstan. Turkey is applying. It is interesting to note that all of these countries are part of the Chinese Belt & Road initiative. As of September 2021, France, Italy, the Netherlands, Germany were also discussing about a possible participation (https://tass.com/science/1343047 and Andrew Jones, “China wants 50 countries involved in its ILRS moon base”, Space News, July 23, 2024, Aedan Yohannan, “China’s space strategy dwarfs U.S ambitions”, The National Interest, March 11, 2024 and Jean-Michel Valantin, “China and the New Silk Road: From Oil Wells to the Moon… and Beyond “, The Red Team Analysis, 6 July, 2015).

The main axis of this cooperation is the construction of the ILSR, officially announced in 2021. Then, in March 2024, the Russian side unveiled the project of building a nuclear power plant, in order to produce enough electricity for the ILSR. This nuclear plant is meant to be built between 2033 and 2035 ( Julianna Suess and Jack Crawford, “Russia and China reaffirm their space partnership”, RUSI, 12 April 2024.

This project is part of the dense space and robotic partnerships that Russia and China are developing. This cooperation deepens since 2017 and the signature of a mammoth deal in space cooperation (Jean-Michel Valantin, “The China-Russian Robot and space cooperation”, ibid ).

In its broad outlines, this deal establishes that China works at modernizing space launchers and spacecraft. Meanwhile, Russia develops robots able to intervene in extreme environments, as outer space. As it happens, for both Russia and China, the development of autonomous robots and probes implies the development of AI. Indeed, this technology is instrumental in the production as well as of the utilization of robots( Valantin, ibid).

The UAE and the asteroids

In the meantime, the United Arab Emirates are preparing the 2028 Emirates Mission to Asteroids. The UAE are a space power (Jean-Michel Valantin, “The UAE Grand strategy for the Future – From Earth to Space”, The Red Team Analysis Society, July 4, 2016). Their robotic probe “Hope” explores Mars since 2021. The goal of this mission is to send a probe that will fly by six asteroids in 2034. Then, it will continue, to orbit around a seventh one. Then, a robot is supposed to land on it (Jeff Foust, “UAE outlines plans for asteroid mission“, Space News, June 3, 2023).

The scientific part of this mission involves a partnership with the Laboratory of Atmospheric and Space Physics of the Boulder University, Colorado (Foust, ibid).As it happens, this partnership may be interpreted as the fact that the UAE need to access to certain levels of technology and scientific capabilities that they cannott yet develop..

What is at stake?

Hence, it is important to establish the strategic complexity of what is at stake in space mining.

The leading BRICS countries in space mining are the UAE, Russia and China. If India is now a space faring nation, its space mining ambitions are not established to this day.

Space mining and national power in space

The R&D and the projection of space mining capabilities on the Moon as well as on asteroids ard also a way to project national power in the solar system. Thus, deep space becomes both the extension as well as the support of national power. Considering AI and industrialization development on Earth space mining could turn the solar system into an immense resources system.

The extraction of those resources will be possible through huge national investments. In other terms, space mining spacecrafts and robots will literally “nationalize” deep space and convert it into spheres of influence. However, this situation may generate discrepancy between those new space practices and the 1967 UN Outer Space treaty. The principles of the treaty establish, among other provisions, that “the exploration and use of outer space shall be carried out for the benefit and in the interests of all countries and shall be the province of all mankind;

outer space shall be free for exploration and use by all States;

So, the appropriation of resources scattered throughout the solar system by space public or private companies may very well have legal and political repercussions. As a result, the national interests that drive the race for mining may well generate important tensions with and within the UN system at the time of its “spatialization”.

Hyper dominance ?

Finally, space mining could become an industrial way to practice dominance from a new definition of (very) “high ground”. Indeed, since 1945 and the start of the race for missiles and for space access, the Earth orbit and the Moon have been eyed by space faring countries as the new place for strategic dominance (William Burrows, This New Ocean, 1998). Thus, having flotillas of spacecrafts and robots in space during the next decade could become a new race for both raw elements and “raw power”.

As was the case, for example, with the interactions between radar, rockets and satellite technologies, that became mutual technological bricks from 1940 to today, space mining is rapidly laying the ground for the new scale of development of space power. This new sequence may very well extend from the Earth towards the asteroid belt ( Neil Sheehan, A Fiery Peace in a Cold War, Bernard Schriever and the ultimate weapon, Random House, 2009).

As it happens, the BRICS momentum to space mining is a race, because it is also a competition with western countries. So, we now need to explore what is geopolitically at stake with space mining in the West.

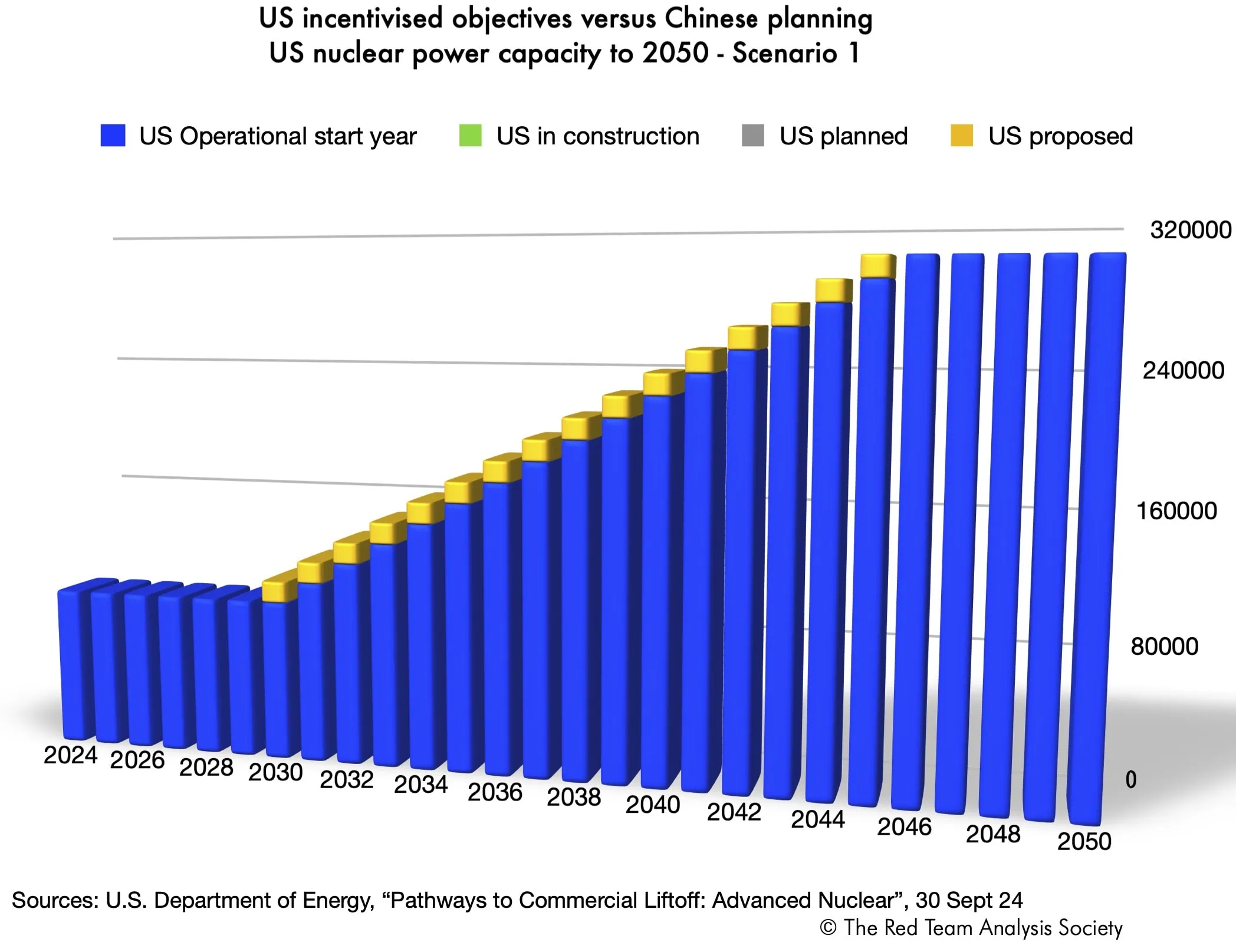

The U.S. has planned for a Nuclear Renaissance. It aims to reach 300 GWe capacity by 2050 for nuclear energy and envisions two scenarios to reach this goal (U.S. Department of Energy -DOE, Pathways to Commercial Liftoff: Advanced Nuclear, 30 September 2024).

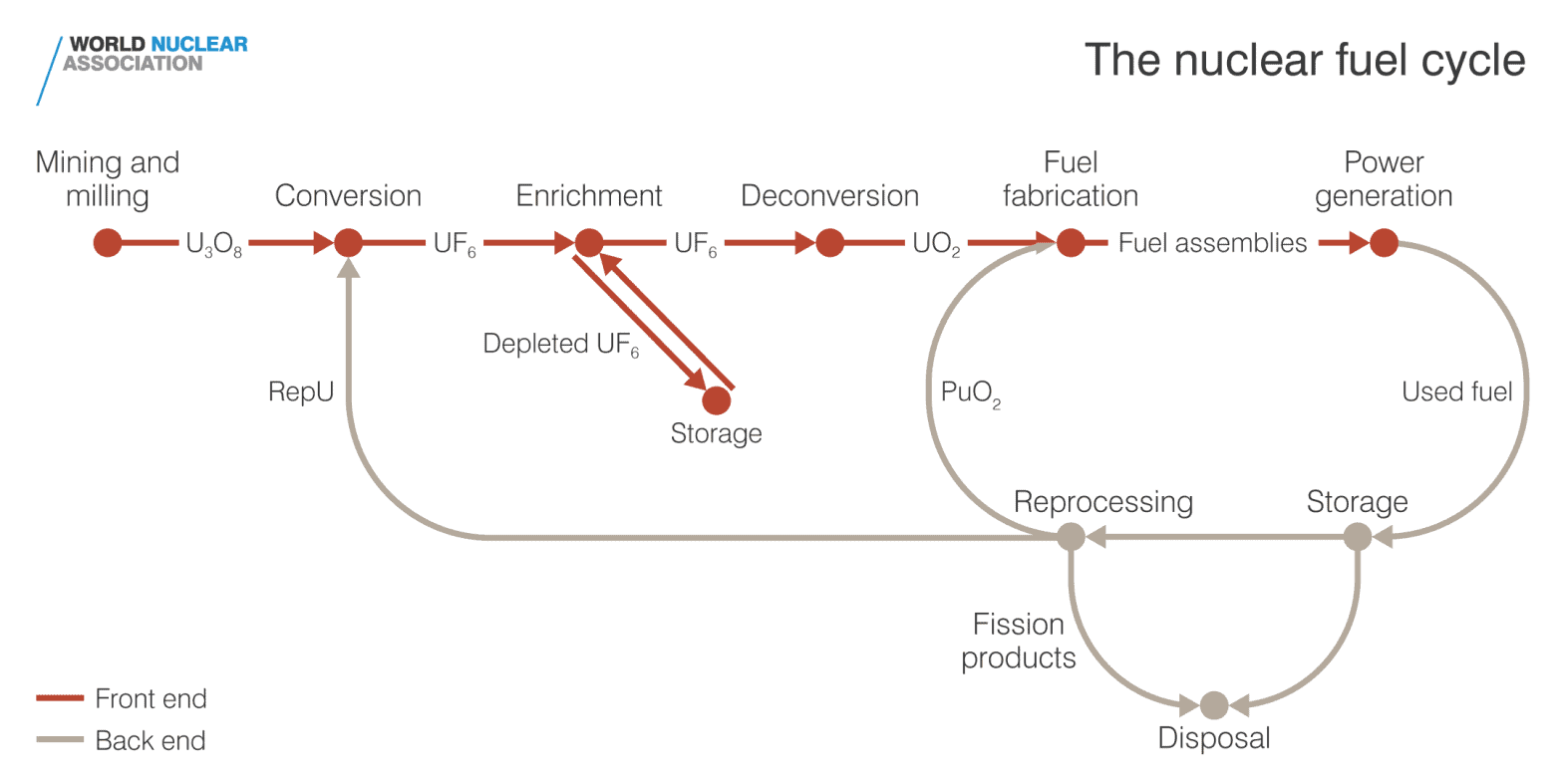

Developing the future American fleet of reactors implies facing formidable challenges and uncertainties (Hélène Lavoix, “Towards a U.S. Nuclear Renaissance?” The Red Team Analysis Society, 15 October 2024). Now, the U.S. must also be able to fuel the nuclear renaissance. This means the U.S. will need first to have uranium, which demands mining it, before even thinking about processing it from conversion to fuel fabrication through enrichment.

How do American nuclear objectives translate in terms of uranium requirements? What does that imply?

In this article we focus on the uranium requirements of the U.S. nuclear renaissance and ways to meet them, including in terms of security of supply. Then, with the next article we shall look at the way the American uranium requirements of the nuclear renaissance and the current supply policy of the U.S. may impact the global uranium field, notably in the light of China’s nuclear surge, with feedback on American options to supply its uranium.

For these two articles we use the DOE scenario 1: nuclear units start being constructed in 2025 for deployment in 2030, and + 13 GWe per year are added from 2030 onwards to reach 300 GW of nuclear capacity for 2050 (US DOE, 2024 Pathways, p. 39).

Scrutinising the U.S. Uranium Requirements

According to the DOE, to meet its objectives, the U.S. would need to “access to ~55.000-75.000 MT per year of U3O8 mining/milling capacity to support 300 GW of nuclear capacity” (Ibid. p.57).

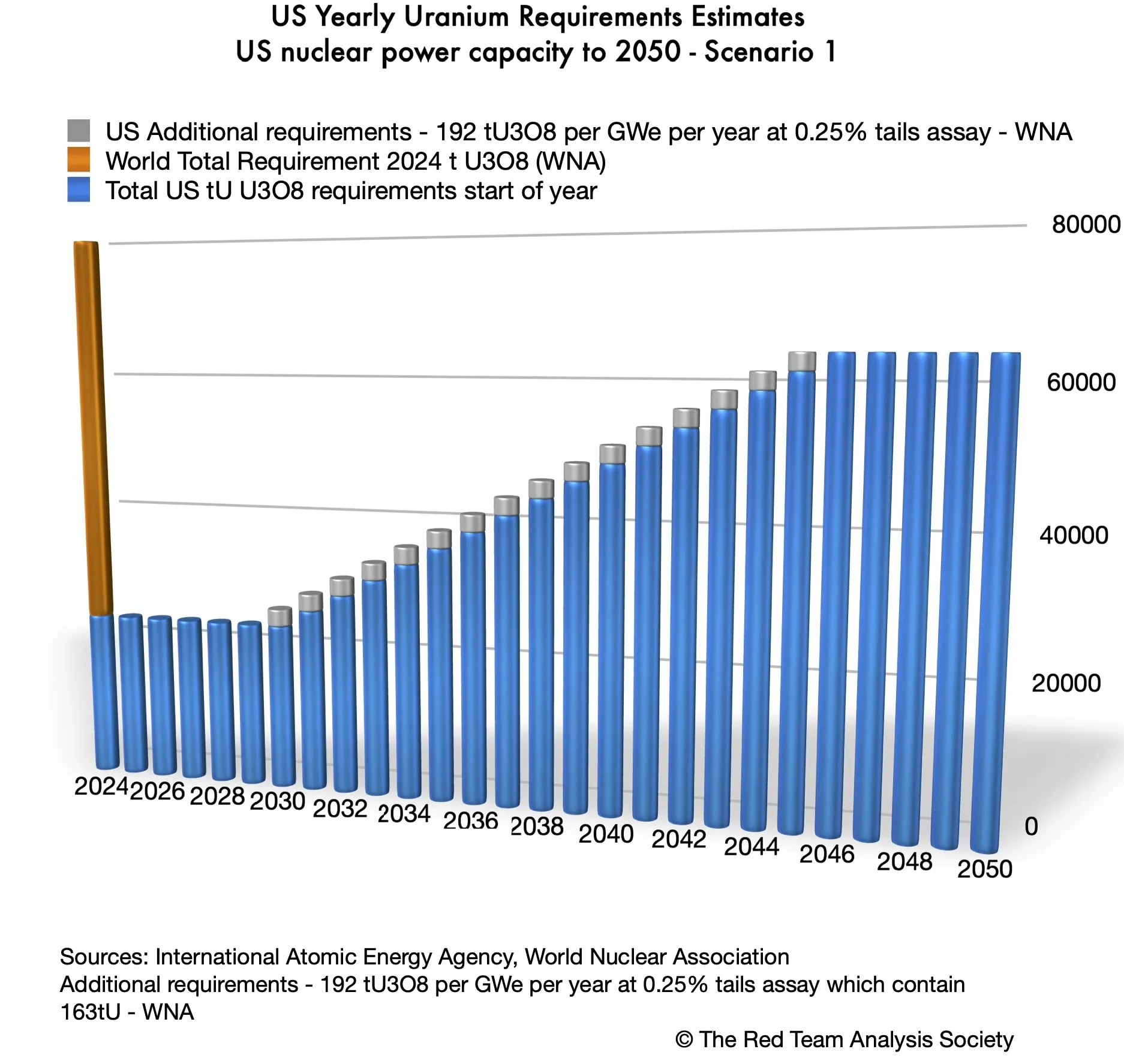

If we assume that all new reactors constructed are at least Gen III(1) (Generation III), then we can consider that the new uranium requirements correspond to 192 tU as U3O8 per GWe per year at 0.25% tails assay (WNA, “Nuclear Fuel Cycle Overview“, May 24).(2)

Thus, the way to 300 GW nuclear capacity through steps of 13 GW per year starting in 2030, as planned for scenario 1, corresponds to an increase in uranium requirements of 2.496 tU as U3O8 per year, starting in 2029-2030. As a result, from 2045-2046 onwards, the U.S. will need to increase, yearly, its supply of uranium to reach at least 61.324 tU as U3O8 per year.

What does that represent exactly, beyond having to meet approximately a tripling of uranium requirements?

The first supplementary deliveries under the form of fuel (and not U3O8) will need to take place for 2030. This means that for the deployment of a nuclear reactor in 2030, the whole fuel cycle will have had to take place before the reactor is loaded for the first test programme, which lasts a couple of months, before connection to the grid. Thus, in terms of timing, we need to take into account that the uranium mined and transformed into yellowcake must then go through the stages of conversion, then enrichment, then fuel fabrication to be loaded on time in a nuclear reactor. This also means transportation. As a result, the requirements presented in the chart below correspond to what is needed for a specific year, not to the time of purchase, which should occur beforehand to allow for the complete fuel fabrication cycle to take place.

For scenario 1, the profile of American uranium requirements could look as shown on the chart below:

Estimates for U.S. Yearly Uranium Requirements – Scenario 1 of the American Nuclear Renaissance

The quantities of uranium that will need to be provided are enormous. From 2045 onwards, they represent approximately 80% of the uranium requirements of the whole world for 2024.

When we compare American uranium requirements to U.S. uranium production, as illustrated in the chart below, the immense challenge of supplying the American Nuclear Renaissance becomes more evident.

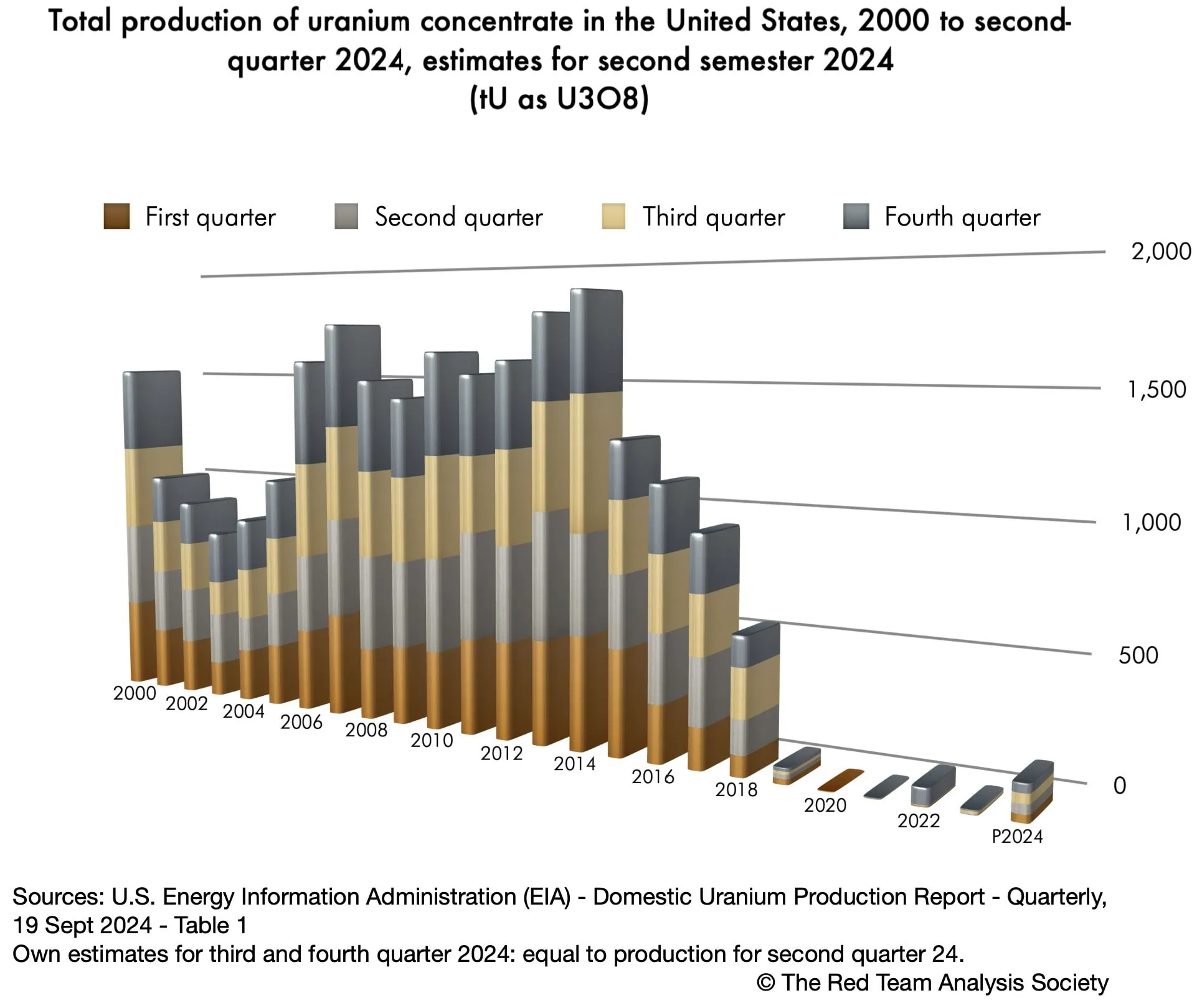

Total production of uranium concentrate (tU as U3O8) in the U.S. 2000 – P2024.

Indeed, at peak in 2014, U.S. uranium production reached 1.881 tU as U3O8 (U.S. Energy Information Administration, Domestic Uranium Production Report, Quarterly 19 Sept 2024, Table 1). Since then it has declined to almost zero with a timid recovery in 2024. Thus, the first supplementary uranium requirement needed for the American nuclear plans already represents 1,33 times the maximum the U.S. has ever been able to produce. Accessorily, the 2014 U.S. peak production is below the 2.000 tU as U3O8 per year of capacity highlighted in the DOE 2024 Pathways (p. 57), to say nothing of the 2019-2024 production.

Currently, without even considering any supplementary nuclear power capacity, the American nuclear requirements represent more than 11 times the U.S. 2014 peak uranium production.

How are the U.S. thus meeting their needs in uranium? Understanding their current uranium supply policy should help us envision how they can meet future needs and the challenges involved.

Purchasing rather than producing uranium

As highlights the DOE, the U.S. “procured ~22.000 MT” (2024 Pathways…, p. 57). This means, obviously, that what the U.S. does not produce domestically is bought elsewhere.

In 2023, the overall amount of uranium delivered to the U.S. was 19.847,8 t U3O8e an increase by 27 % on the 2022 amount. This increase may correspond to the connection to the grid of the Vogtle reactors, or to a lesser use of uranium stored, or both. It represented 93,27% of the U.S. requirements for 2023 (WNA, World Nuclear Power Reactors & Uranium Requirements, Dec 2023).

A reduced American involvement in uranium mining, at home and abroad

The U.S. faces a double challenge, as revealed by the next two charts.

Insufficient uranium deposits on American territory

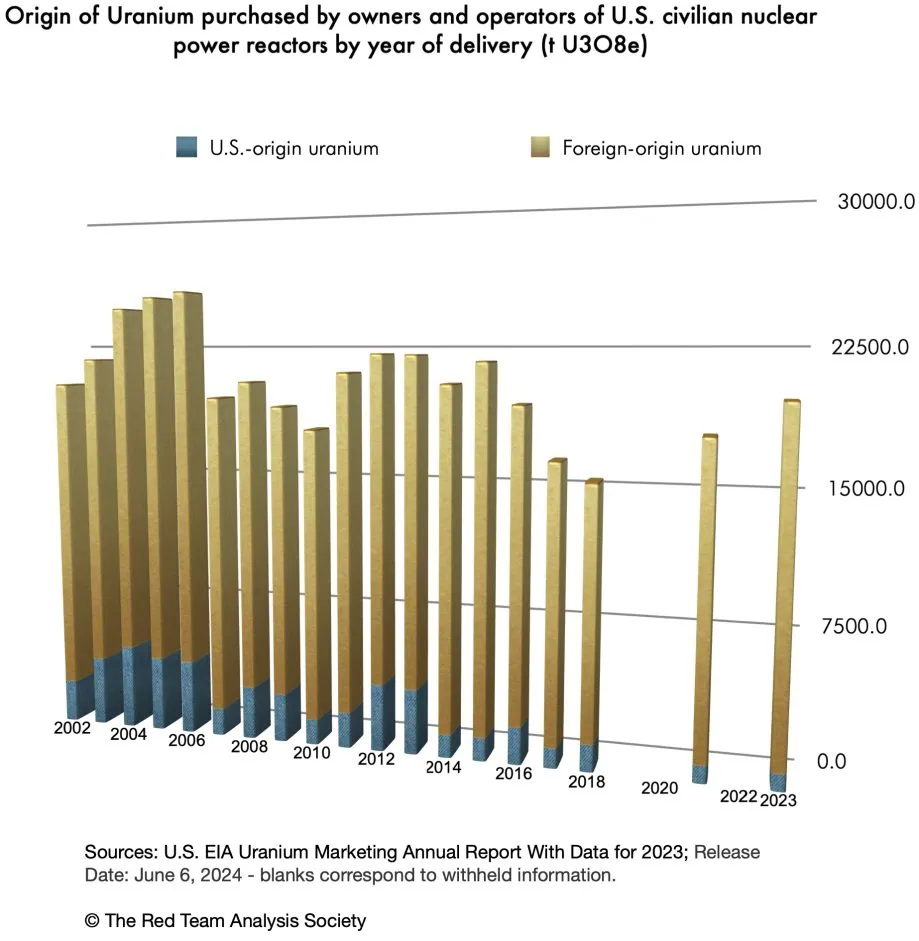

First, as expected from the uranium production figures, only 4,65% of the uranium delivered originated from the U.S., i.e. came from American deposits, whilst 95,35% came for foreign countries (first chart). The American situation compared with the early 2000s worsened, as uranium production has plummeted since 2016.

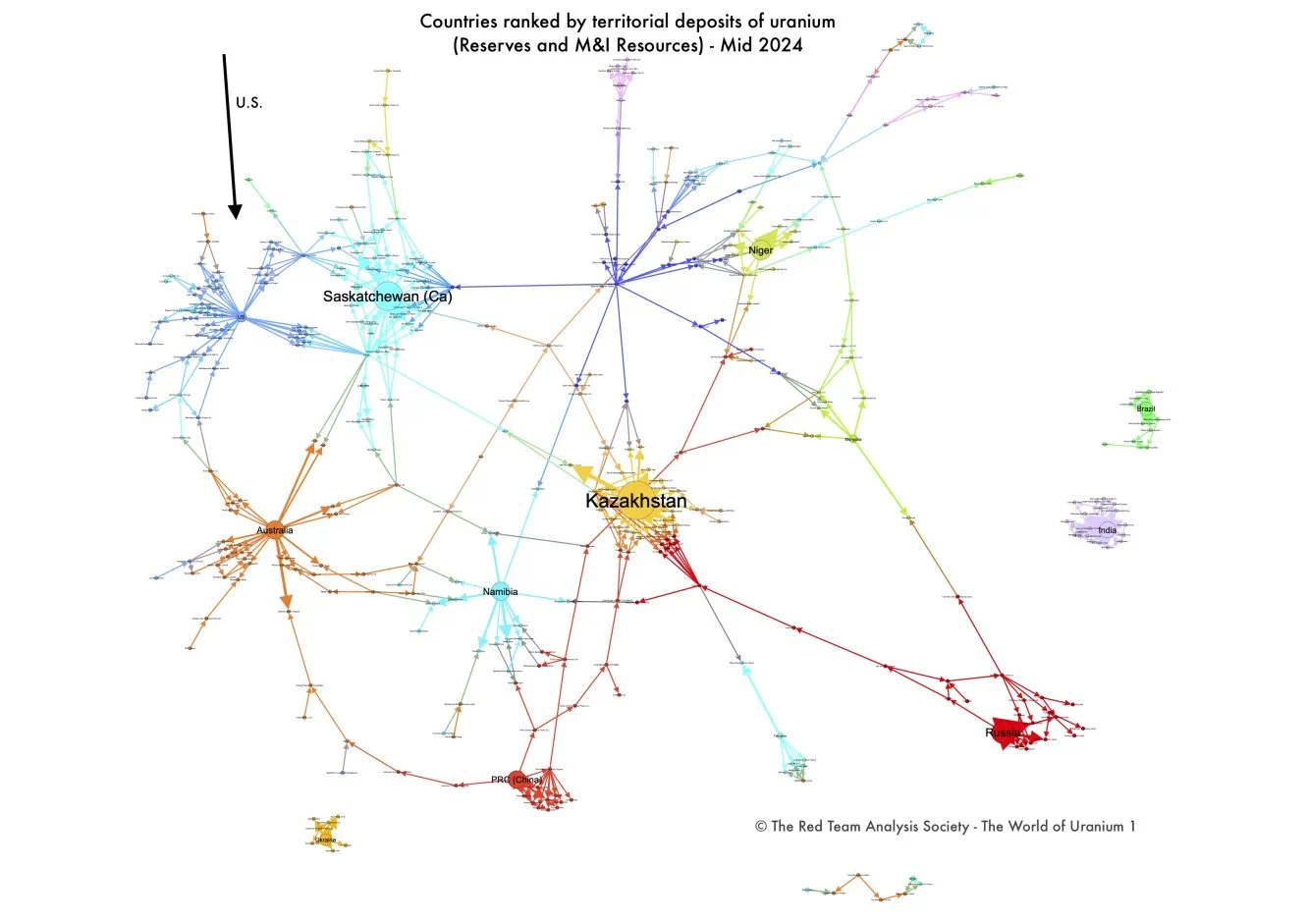

Indeed, compared with all other uranium producing countries, the U.S. is far from leading in terms of uranium reserves and resources. If we add the reserves and measured and indicated resources of 126 mines worldwide with known such reserves and resources, then the U.S. ranks 12th for the deposits on its geographical territory (see The World of Uranium – 1: Mines, States and Companies – Database and Interactive Graph).

Countries ranked by territorial deposits of uranium (Reserves and M&I Resources) – Mid 2024 – Source: The World of Uranium 1 – (Preview)

These deposits, when adding all the assessed mines on American territory, amount nonetheless to 147.820 tU as U3O8 (Ibid.). Yet, this corresponds only to 6,77 years of uranium requirements for 2023, and to 2,41 years of uranium requirements from 2045-2046 onwards.

Overwhelming reliance on foreign suppliers

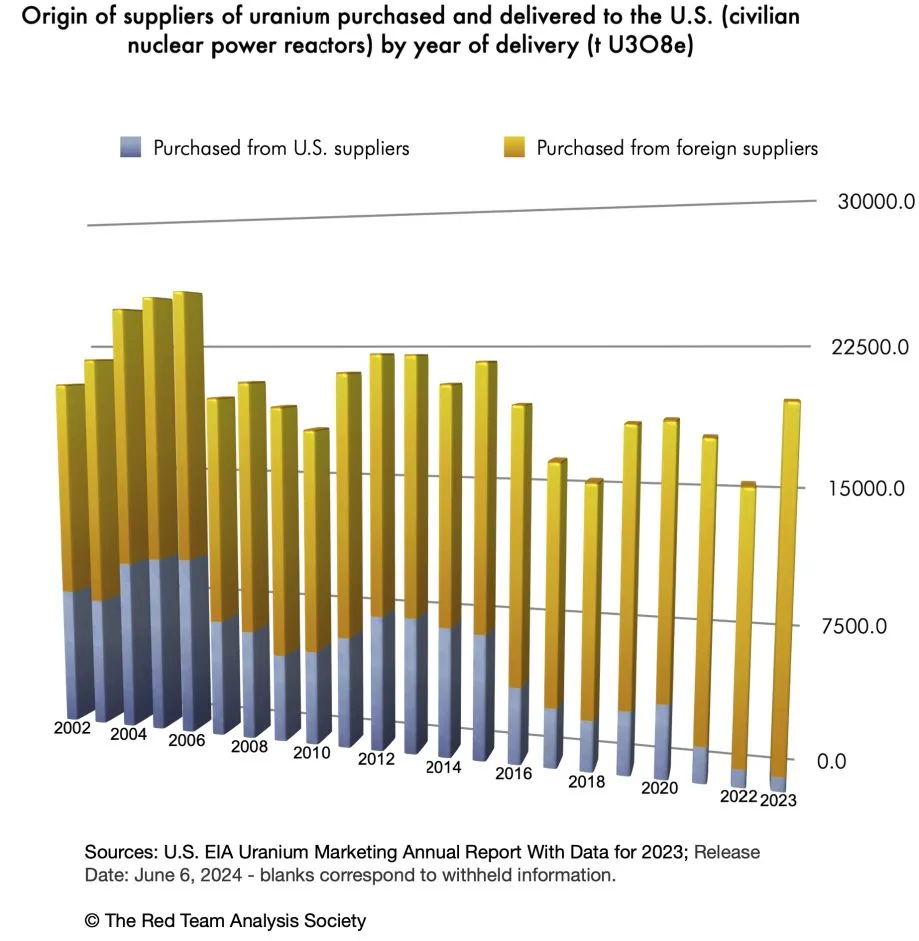

Secondly, only 3.88% of the uranium delivered to the United States was purchased by American suppliers, whilst 96.12% was purchased by foreign suppliers (second chart). The situation, again, has considerably worsened throughout the first two decades of the millenium, showing a disinterest of American companies in uranium.

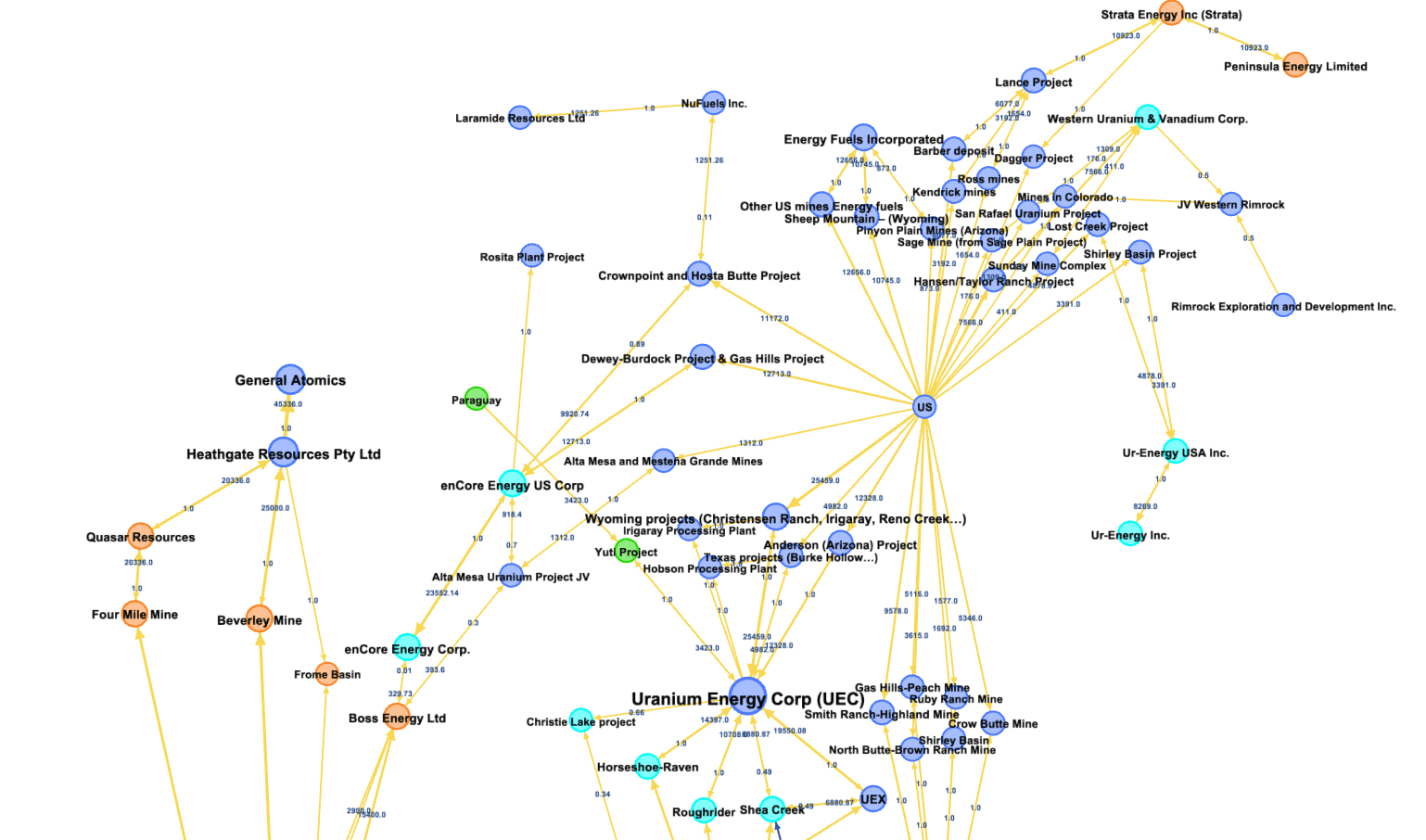

Moreover, the two charts above together show that not only U.S. domestic production is small, but, it is also partly done by foreign companies, which is confirmed by the graph below (created with the World of Uranium – 2). Indeed Australian and Canadian companies hold shares of American uranium deposits.

The web of U.S. Uranium Mining companies and shares of reserves and resources (Blue = U.S., Orange = Australia, Turquoise = Canada; Green = Paraguay) – Screenshot of part of the graph of the World of Uranium – 2 (overview/filtered).

Meanwhile, American mining companies hold, worldwide, relatively few reserves and resources. As they have been little involved overseas, apart from some mines held in Paraguay, Australia and Canada, their share of overseas reserves and resources is relatively not very important (see The World of Uranium – 2: Mines, States, Companies and Shares of Reserves and Resources – Database and Interactive Graph).

Dependence on foreign companies and foreign supply for uranium

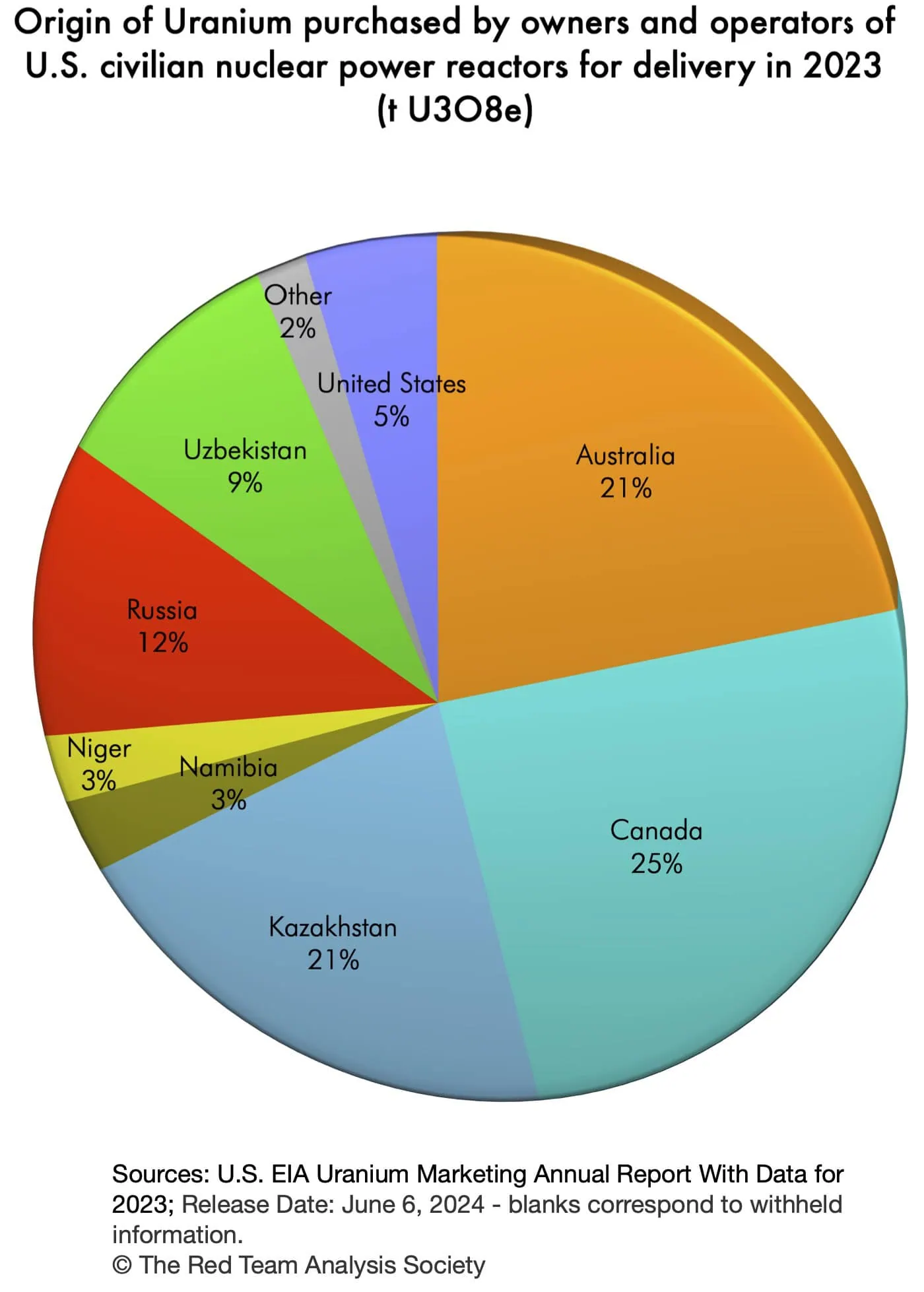

As a result, with little production either at home or abroad, the United States relies abundantly on purchase from foreign companies of uranium mined abroad, mainly through long-term contracts (84,08% in 2023) and on the spot market (14,92% in 2023) (U.S. Energy Information Administration, “Table S1a. Uranium purchased by owners and operators of U.S. civilian nuclear power reactors, 2002-2023”, 2023 Uranium Marketing Annual Report, June 2024).

The countries from which the uranium delivered in 2023 was purchased are as shown on the chart below:

Origin of uranium purchased by owners and operations of U.S. civilian nuclear power reactors for delivery in 2023

As we shall now see this American dependence on foreign uranium and foreign operators fragilise the security of uranium supply of the U.S. in the light of global politics.

When dependence on foreign uranium fragilise the security of uranium supply

Losing Russia and Niger’s uranium?

Assuming the new 2025 Trump administration does not change 2024 policies and does not work its way towards mending relationships with Russia, by 1st January 2028 and the end of the Russian sanctions waiver regime, Russia should not be anymore a source for uranium for the U.S..

Actually, considering the Russian decision to temporarily ban the export of enriched uranium to the U.S., with exceptions according to Russian interests, the necessity for America not to rely on Russian uranium could be far closer in time, if not immediate (Jonathan Tirone, Ari Natter and Will Wade, “Russia takes aim at US nuclear power by throttling uranium“, Mining.com, 15 November 2024).

The need to replace Russian uranium could also last “only” as long as American policy towards Russia does not change, while being a stake among others in possible future changes of relationships between the U.S. and Russia.

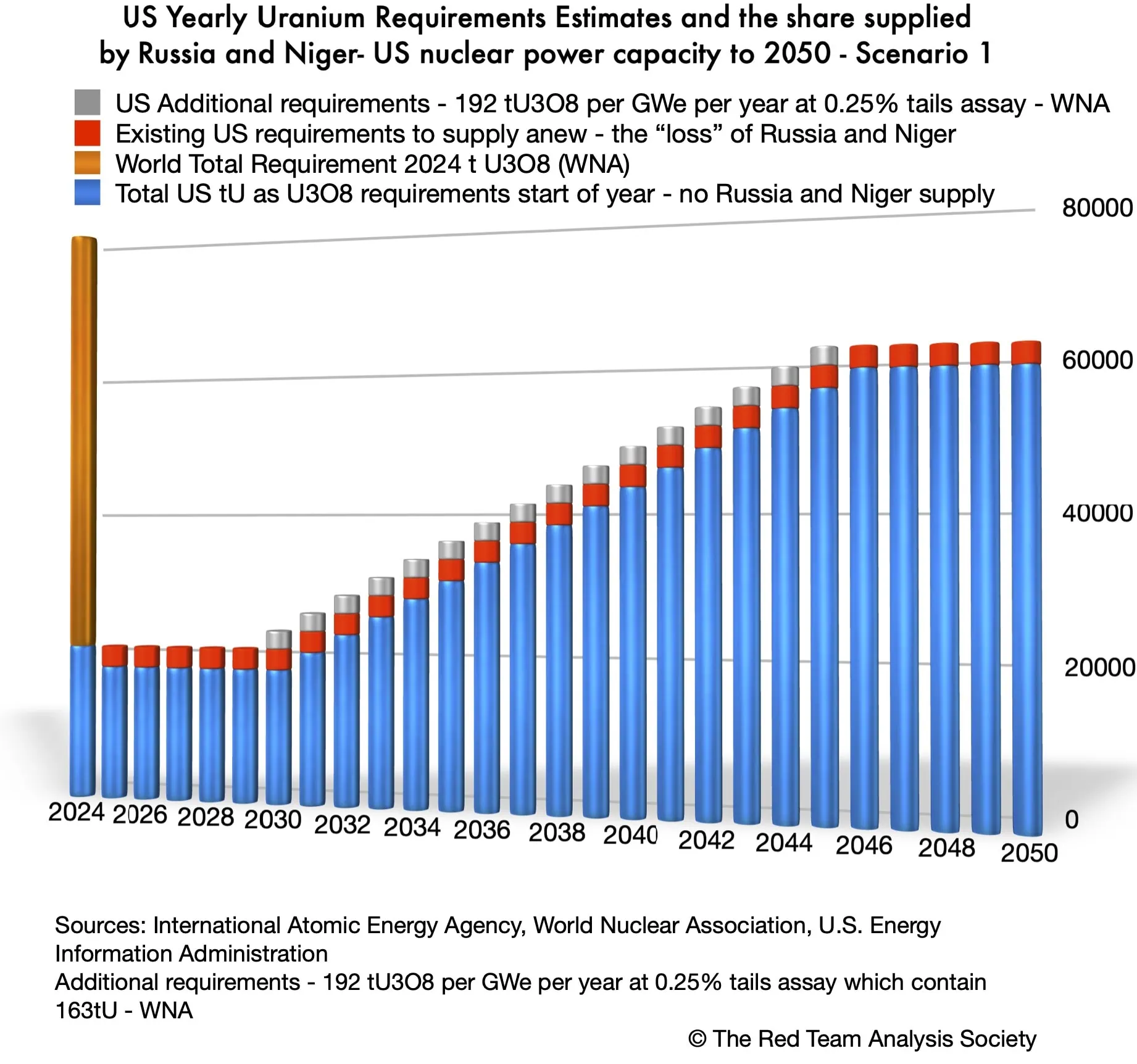

Hence, always in the hypothesis of a continuation of the Biden administration’s policy toward Russia by the Trump administration, on top of the future requirements needed for its Nuclear Renaissance, the U.S. may also need to secure yearly 2.869 tU as U3O8 to replace Russian and Nigerien uranium (U.S. Energy Information Administration, “Table 3. Uranium purchased by owners and operators of U.S. civilian nuclear power reactors by origin country and delivery year, 2019–23”, 2023 Uranium Marketing Annual Report, June 2024).

More exactly, suppliers of uranium for American requirements need to secure every year these 2.869 tU as U3O8.

Increasing uranium requirements while shrinking the possible sources of supply

As a result, even though the requirements supplied previously by Russia and Niger are not new, they will nonetheless have to be met in a new way. It is thus 2.869 tU as U3O8 yearly the U.S. has to procure newly until 2029, to which will be added then the supplementary 2.867 tU as U3O8 each year, corresponding to the added nuclear capacity of scenario 1. Thus, on the one hand requirements have increased, while on the other hand the available supply has shrank as Russian and Nigerien deposits are not anymore available, until conditions and policies change.

The American requirements, which thus have to be supplied, are shown on the chart below:

Estimates for U.S. Yearly Uranium Requirements showing the share supplied by Russia and Niger – Scenario 1 of the American Nuclear Renaissance

To illustrate the purchases the U.S. would have to make to supply these new American uranium needs for Scenario 1, we may separate certain requirements – those that were supplied by Russia and Niger – from possible ones, stemming from the plans for the nuclear renaissance.

Replacing uranium from Russia and Niger

The yearly 2.869 tU as U3O8 requirements that were previously supplied by Russia and Niger, may now come from the increase in production planned by Canadian Cameco and French Orano for their plants of Cigar Lake(3)and McArthur River/Key Lake(4) (for more on these companies see, Helene Lavoix, “Revisiting Uranium Supply Security (1), The unique world of those who mine uranium“, The Red Team Analysis Society, 21 May 2024). If we look for these plants at the production for 2023 and compare it with the expected production for 2024, the increase in production for the two sites corresponds to 2.847 t U as U3O8, which is approximately what is needed to cover the American needs to replace Russia and Niger. In this hypothesis, we imagine that the partners for the two mines and mills sell all the supplementary production to the U.S..

In 2038 and 2041, however, these mines will have reached the end of their lives and other sources of supply will have to be found.

Meanwhile, as we shall see in the next article, where we shall consider the impact of the American uranium requirements on the global uranium stage and then feedback on uranium supply, not all production of these mines may be sold to the U.S.. In that case, some American nuclear utilities would have to find elsewhere other sources of supply. At worst they could be left without enough uranium to power their reactors, which could mean electricity shortages.

Procuring for the new uranium requirements of the American nuclear renaissance

The main existing producing mines and mills of Canada have already been used in our hypothesis to replace Russian and Nigerien uranium (Canadian Nuclear Safety Commission, Operating uranium mines and mills – Rabbit Lake is currently under safe state of care and maintenance and 14.847 tU of indicated resources remain).

The U.S. will thus need to procure uranium elsewhere. This demands starting operations in new mines, as we shall see with the next article.

Now, each year, the new supplementary needs of the U.S. stemming from scenario 1 would represent the equivalent to between 10.6% and 11% of the entire 2024 Kazakh production, which should reach between 22.500 and 23.500 tU (update to 2024 production guidance, “Kazatomprom 1H24 Financial Results and 2025 Production Plan Update“, 23 August 2024). Kazakhstan is the first producer of uranium in the world.

This means that for 2030 the U.S. would need the equivalent to 10.6% to 11% of the Kazakh production. Then for 2031 it would need another 10.6% to 11%, thus it would absorb the equivalent to between 21.2% and 22% of the Kazakh production. For 2032 it would again need another 10.6% to 11%, thus would absorb the equivalent to between 31.8% and 33% of the Kazakh production, etc.

From 2045 onwards each year, considering the entirety of American requirements, the U.S. would swallow the equivalent of almost thrice the entire 2024 Kazakh production. The U.S. will thus have to “find three Kazakhstan” every year for ever or for as long as its nuclear energy capacity remains at 300 GWe.

These are unprecedented quantities.

Now, uranium mining, production, and trade are activities taking place at a global level: actions at one end of the planet by one player impact the whole uranium playing field, which in turn has consequences for each and every actor. Thus, before to look at options available to the U.S. we must first contextualise globally American uranium requirements: Uranium for the U.S. Nuclear Renaissance – 2: Towards a global geopolitical race.

Notes

(1) Advanced nuclear reactors include Generation III (Gen III), Generation III+ (Gen III+) and Generation IV (Gen IV) reactors (see for example, WNA, “Advanced Nuclear Power Reactors“, April 2021).

(2) These estimated requirements in uranium are a minimum. Indeed, if a reactor of an older technology is recommissioned, as is likely to be the case, then uranium requirements will be higher (for a rapid summary regarding the generations (GEN) of reactors and recommissioning, Lavoix “Towards a U.S. Nuclear Renaissance?“).

(3) Cigar Lake is owned at 54.547% by Cameco, 40.453% by Orano Canada Inc. (Orano) and 5% by TEPCO Resources Inc.

(4) The Key Lake mill is owned 83.333% by Cameco and 16.667% by Orano.

At the end of October 2024, the Ecole Supérieure des Forces de Sécurité Intérieure (ESFSI) of the Home Ministry of Tunisia organised the first session of its fifth intensive training on early warning systems & indicators.

This session ran concurrently with a crisis management module, highlighting the interconnected nature of the two disciplines. First, if a warning system fails, a crisis ensues, requiring immediate crisis management decisions and actions. The job of the early warning module is thus to train senior officers to have to use as rarely as possible what is taught in the crisis management module, yet to be ready to do so. Second, as a crisis is managed through decisions and measures, it is crucial to anticipate potential future threats or hazards that may emerge as a consequence of the very management of the crisis. This includes grappling with the intricate domain of unintended consequences. Therefore, comprehending the concept and fundamentals of warning and effectively integrating warning systems and analyses into the crisis management process is essential.

For the October and November session of the training in early warning and indicators, Dr Hélène Lavoix trained senior officers in an intensive 35-hour programme focusing on fundamentals, processes, analysis and practice on issues of interest.

As always the many in-depth and extremely interesting discussions with the trainees and the executive management of the ESFSI, to say nothing of their amazing hospitality, transformed this week in a high level, high quality workshop.